The delivery numbers themselves don't have any major negative surprises, but other developments are hurting stocks, including the Nvidia chip ban and the Chengdu Covid lockdown.

China's major electric vehicle (EV) makers reported mixed August deliveries on September 1, and in the view of Deutsche Bank analyst Edison Yu's team, they were better than many had previously feared, but note that new concerns are beginning to surface.

US-listed Nio, Xpeng, and Li Auto all plunged Thursday after the deliveries were announced, down 5.63 percent, 6.43 percent, and 3.02 percent, respectively.

Yu's team doesn't see any major negative surprises in the delivery numbers themselves, but said other developments yesterday are hurting these stocks, including the Nvidia chip ban and the Chengdu Covid lockdown.

Here's the team's take on the deliveries of what they call the "Fab 5" EV makers -- Nio, Xpeng, Li Auto, Zeekr, Hozon.

Aug sales better than feared but new concerns emerging

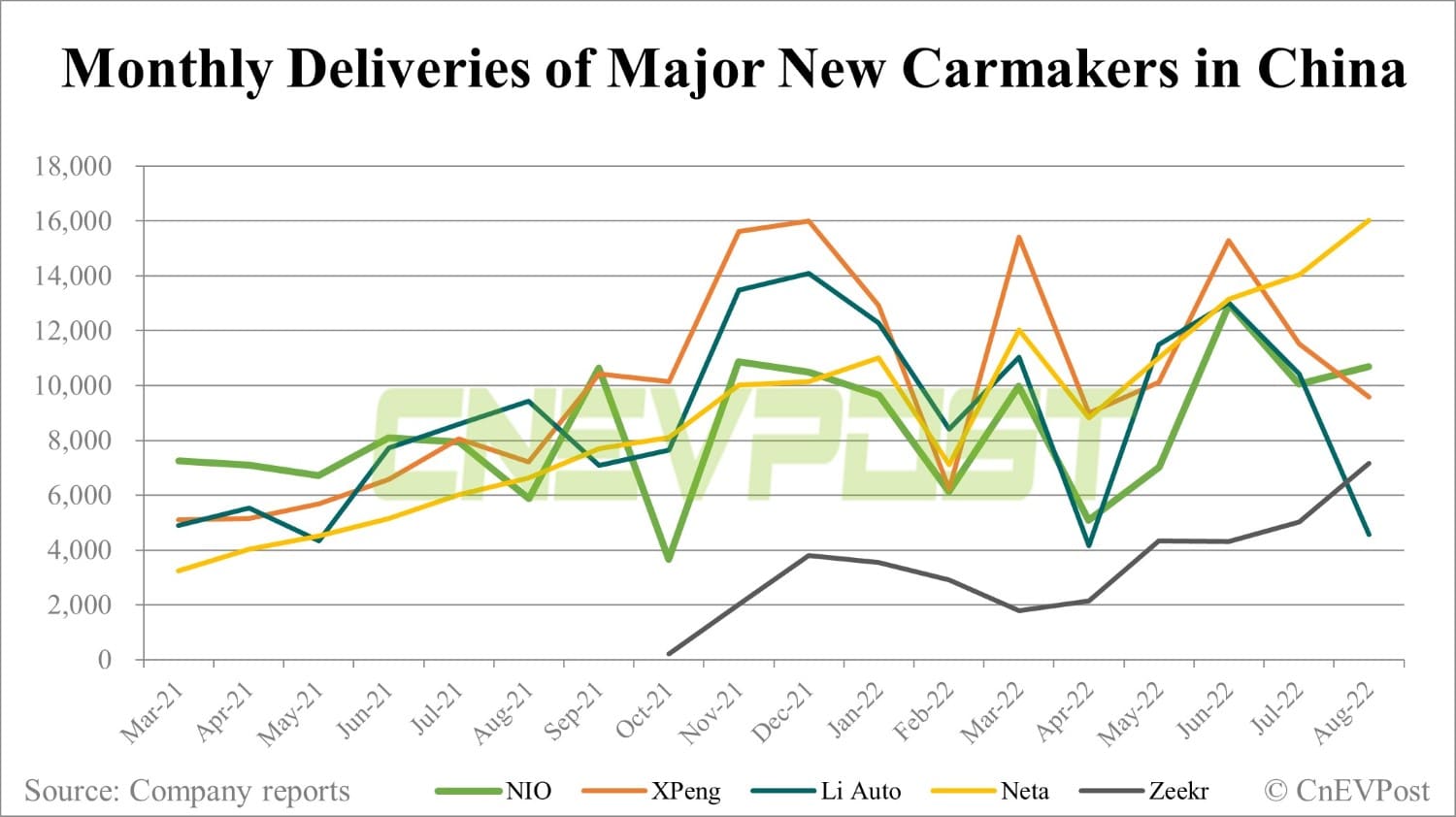

Fab 5 China EV sales came in mostly better than expected in August following a weak July.

Nio delivered upside while still being constrained by a casting parts shortage; its older models are showing resilience and the new ES8 appears to be ramping very strong out the gate.

Li Auto saw weak sales as anticipated due to L8/ L9 transition. Xpeng volume was about in-line. Zeekr once again saw strong demand with record deliveries and order book performance; Hozon Neta also set a record selling month.

While we didn't see any major negative surprises with August sales, we do believe other developments are hurting the stocks today including the Nvidia chip ban (supplier for Nio, XPEV, and LI) and Chengdu COVID lock down (>21m people).

August EV sales

Nio delivered 10,677 units (+6% MoM; +82 YoY), beating our forecast. Flagship ET7 sedan deliveries were better than feared at 3,126 but were still hurt by supply shortage of casting parts (nearly 2,000 unit drag in our view).

ES8 began deliveries on 8/28, garnering 398 units in the month, better than we expected, putting it on track for solid uptick in Sep (we had only modeled 1,000 units).

Gen-1 "866" sales were only down slightly MoM, suggesting Nio's premium branding focus is perhaps more resilient to emerging competition as previewed.

Xpeng delivered 9,578 units (-17% MoM; +33% YoY) in August, in line with our forecast. All 3 models showed some sequential decline with P7 coming in better than expected while P5 came in worse. See our latest report Making multiple painful pivots for detailed thoughts following 2Q22 earnings.

Li Auto delivered only 4,571 units (-56% MoM, -52% YoY), coming in slightly below our forecast. We continue to believe demand for the new L9 full-size SUV is strong but deliveries were delayed in August due to a range extender supply issue caused by power curbs in Sichuan province. This means that L9 volume was likely even lower than we had anticipated.

Separately, Li Auto confirmed the smaller L8 SUV will begin deliveries in November, slightly later than we're modeling. The model will be available in two trims, a six-seater and a VIP five-seater, representing a departure from the company's strategy of offering just one standard SKU.

Zeekr delivered impressive August sales at 7,166, up from July's 5,022. Order intake was above 10,000 again (record level) with ASP >336,000 RMB.

We test drove the 001 in Oslo in July and found it to be a very appealing product with an unique style ("shooting brake" design). This could be helping the vehicle differentiate from the competition.

Hozon sold 16,017 units of its Neta-branded BEVs (+14% MoM; +142% YoY), setting a record for a second consecutive month.