Edison Yu's team expects China NEV sales momentum to pick up in November and December, when a host of new models should drive sales to new highs and NEV subsidies are poised to exit.

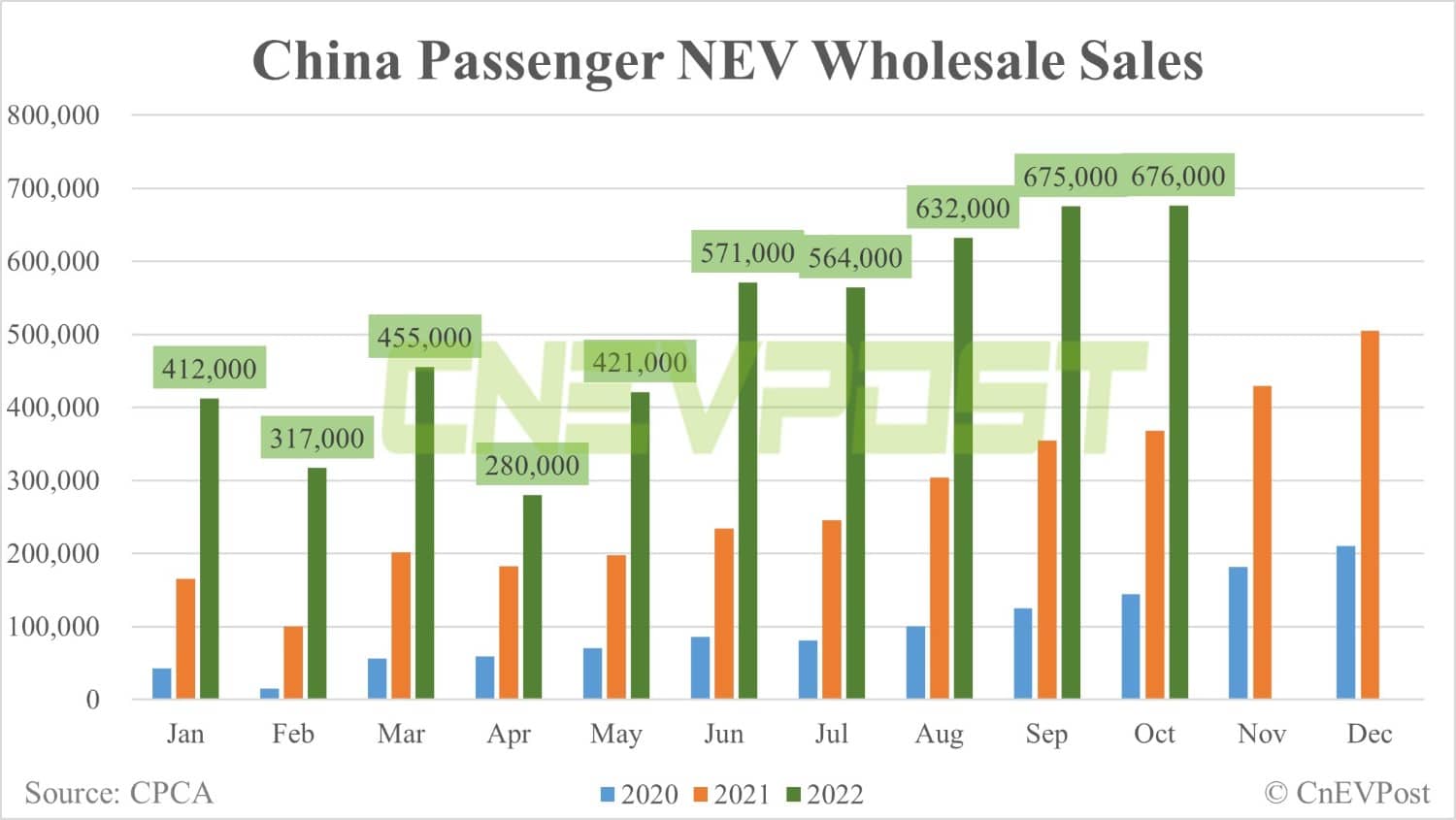

Wholesale sales of new energy vehicles (NEVs) in China reached 676,000 units in October, continuing to reach record highs despite the impact on residential spending due to Covid, according to data released yesterday by the China Passenger Car Association (CPCA).

Despite concerns about weak consumer sentiment, China's electric vehicle sales were quite strong in October, Deutsche Bank analyst Edison Yu's team said in a research note sent to investors on Tuesday.

The team expects sales momentum to pick up in November and December, when a raft of new models should drive sales and penetration to new highs and NEV subsidies are poised to exit.

Yu's team continues to expect full-year NEV sales in China to reach 5.7 million units, implying a 92 percent year-on-year increase.

Looking ahead to 2023, NEV sales in China could depend on what happens with Covid, the team noted.

If lockdown measures remain very strict, China's NEV sales could see a downside to the low 7-million-unit range, according to the team.

If the government opens up, even gradually, China's NEV industry will easily see demand for more than 8 million units as many attractive new models enter the market, especially at the premium end, Yu's team said.

Wholesale sales of battery electric vehicles (BEVs) in China were up 67.7 percent to 508,000 units in October, accounting for 75 percent of all NEV sales, according to data released yesterday by the CPCA.

Wholesale sales of plug-in hybrid vehicles (PHEVs) were 167,000 units in October, up 157 percent year-on-year.

In October, both China's NEV and traditional internal combustion engine vehicle markets were impacted by Covid control measures in some regions, which left September and October, traditionally the peak sales season, relatively flat, the CPCA said.

Here is the full text of Yu's team's research note.

Oct shows secular shift intact despite weak consumer

October industry EV sales came in fairly strong despite concerns around weak consumer sentiment.

According to the CPCA, BEV retail volume was 397k or -60k units sequentially (which is essentially equivalent to Tesla's MoM retail decline as it prioritized exports).

PHEV retail sales came in at a record high of 159k units, taking overall NEV sales to 556k or 30% industry penetration (in-line with CPCA's prior commentary).

Production and wholesales were both about flat MoM.

Looking ahead, we expect sales to pick up momentum in Nov/Dec when a host of new models should drive volume/penetration to new highs (e.g., ET5, L8+L9, G9, Neta S) and NEV subsidy prepares to roll-off.

We continue to expect full-year NEV sales to come in at 5.7m units (+92% YoY).

Looking at 2023E, we think volume will likely depend on the COVID situation. Should lock-downs remain very stringent, we could see downside to the low 7m range.

If the government opens up, even on a gradual basis, we think there is easily demand for >8m units as many new attractive models come to market especially on the premium end.

October OEM recap

Tesla sold 17,200 vehicles at the retail level and exported 54,504 units, adding up to wholesales of 71,704 (41,488 Model Y + 30,216 Model 3).

Nio delivered 10,059 units (-8% MoM and +174%YoY). The Hefei govt locked down areas of the city and Nio experienced high volatility getting certain parts and workers to come in (e.g., paying extra for workers to be closed-loop when possible).

This has held back ET5 volumes in particular (only ~1,000 units delivered during Oct). ET7 sedan sales were 3,050 units, still dragged down by casting supply but going forward should improve after qualifying more suppliers. ES7 saw healthy MoM increase in volume to 2,814 units. See our 3Q earnings preview here.

Li Auto delivered 10,052 units(-13% MoM, +31% YoY), in-line with our expectations and likely better than feared. The volume in the month was heavily back-end loaded.

Xpeng delivered 5,101 units (-40% MoM; -50% YoY), below our forecast. Sales continue to struggle across all models as focus turns to G9 ramp which sold 623 units in the month (mass production began on 10/27); this should increase materially in Nov/Dec, taking 4Q to at least 10,000 units. The company also is wrapping up a organizational restructuring as a result of the poor sales performance in recent months.

Zeekr delivered record monthly sales again at 10,119, up from September's 8,276 as demand for the uniquely styled 001 remains robust (ASP >336k RMB). Zeekr also unveiled its upcoming premium MPV called 009, equipped with CATL's new Qilin battery that can deliver >500 miles of range using a 140 kWh pack.

Hozon sold 18,016 units of its Neta-branded EVs (flat MoM; +122% YoY). Huawei-backed AITO sold 12,018 units (+19% MoM), setting a new monthly record.