Li Auto's management could achieve its goal of transitioning from EREV to BEV, but the road ahead could get much rockier, said Edison Yu's team.

Deutsche Bank analyst Edison Yu's team lowered their price target on Li Auto further, just less than 10 days after the last cut, as second-quarter earnings made them more cautious about the company.

In a research note sent to investors today, Yu's team lowered its price target on Li Auto to $28 from $30, after cutting it to $30 from $32 on August 9.

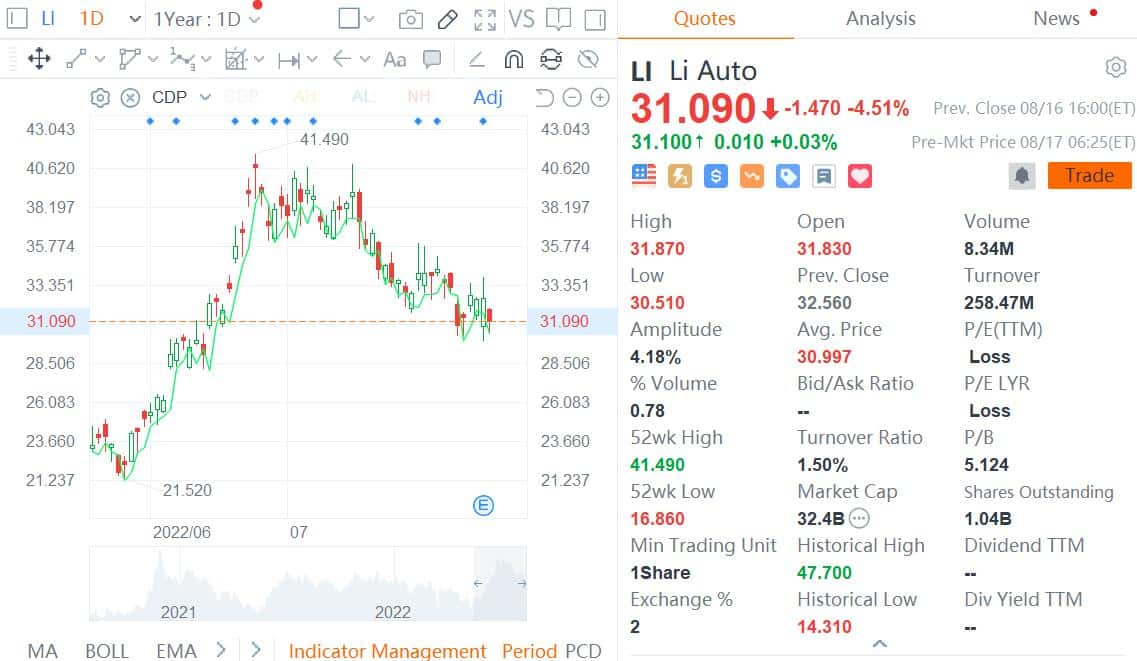

Li Auto closed down 4.51 percent to $31.09 on Tuesday in the US, and the latest price target implies a 10 percent downside.

The automaker reported solid second-quarter earnings on August 15, but guidance for the third quarter was weak.

"Coming out of earnings, we become incrementally more concerned about Li Auto's longer term prospects," the team wrote.

Li ONE sold 13,000 units in June, but could be as low as 4,000-5,000 units by this month and next without experiencing any sort of supply chain bottleneck.

Li Auto now has to rapidly deploy new models to properly attack the ever-changing EV market. However, the company is clearly relying more on EREVs than BEVs for sales growth in the coming years, Yu's team noted.

This has helped improve profitability, but Li Auto's management risks missing the "forest for the trees," according to the team. They further states:

EREV has always been a stop-gap approach (possessing little strategic technological value in our view), not an end-game solution.

Should this really be the centerpiece of a company's roadmap for the next few years as aggressive BEV competition emerges?

We think perhaps not and frame this in the context of Nio having >1k swap stations and in-sourcing battery cells, and attempting to cultivate a local ecosystem in Europe which represents a large and relatively less competitive market for EVs.

The team lowered their forecast for Li Auto's full-year deliveries this year from 160,000 to 140,000 to account for much lower sales of the Li ONE.

Looking ahead to 2023, the team believes Li Auto is expected to launch another EREV model called the Li L7 (X03) by the end of the second quarter, expanding its model lineup to three EREV SUVs.

The team expects production capacity for the Li L8 and Li L9 to be 20,000-25,000 units per month, operating in two shifts. After production of the Li ONE is phased out, the company will convert that capacity to the L-Series, worth at least 15,000 per month.

Yu's team lowered their BEV sales forecast for the Shark (high performance SUV) and the Whale (luxury MPV) because Li Auto plans to adopt a very high-end pricing strategy to maintain gross margins.

The team does not believe Li Auto will offer the same level of value for BEVs as it does for EREVs, which could limit initial demand.

The team reduced their forecast for Li Auto deliveries in 2023 by 10,000 units to 265,000, but increased their gross margin forecast by 1.3 percentage points to 23.1 percent.

Yu's team believes Li Auto's management can achieve its goal of transitioning from EREVs to BEVs, but the road ahead could get much rockier.

The team lowered its price target by $2 to $28, still based on a 3.0x 2023 EV/Sales.