Deutsche Bank believes the true test for Li Auto will come in the second half of the year.

Li Auto (NASDAQ: LI) saw strong deliveries in the fourth quarter, and with it set to report quarterly results next week, its performance will be something to look forward to.

"Li Auto is the best performing China EV stock so far this year which is well deserved in our view," Deutsche Bank analyst Edison Yu's team said in an earnings preview sent to investors yesterday.

Li Auto said last week that it will report financial results for the fourth quarter and for the full year 2022 on Monday, February 27, before the US stock market opens.

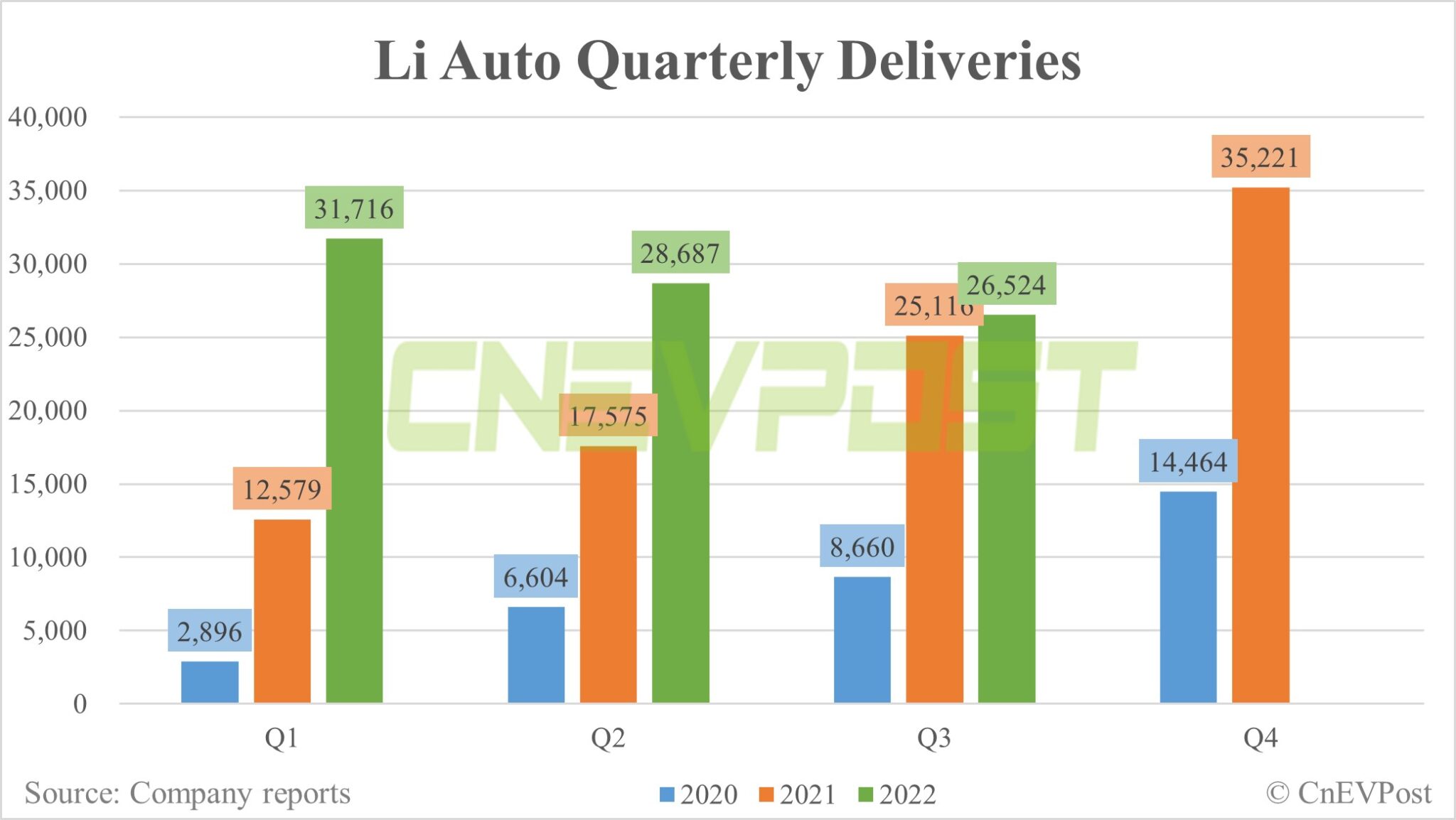

Li Auto has previously reported that it delivered 46,319 vehicles in the fourth quarter, within the guidance range of 45,000 to 48,000 vehicles.

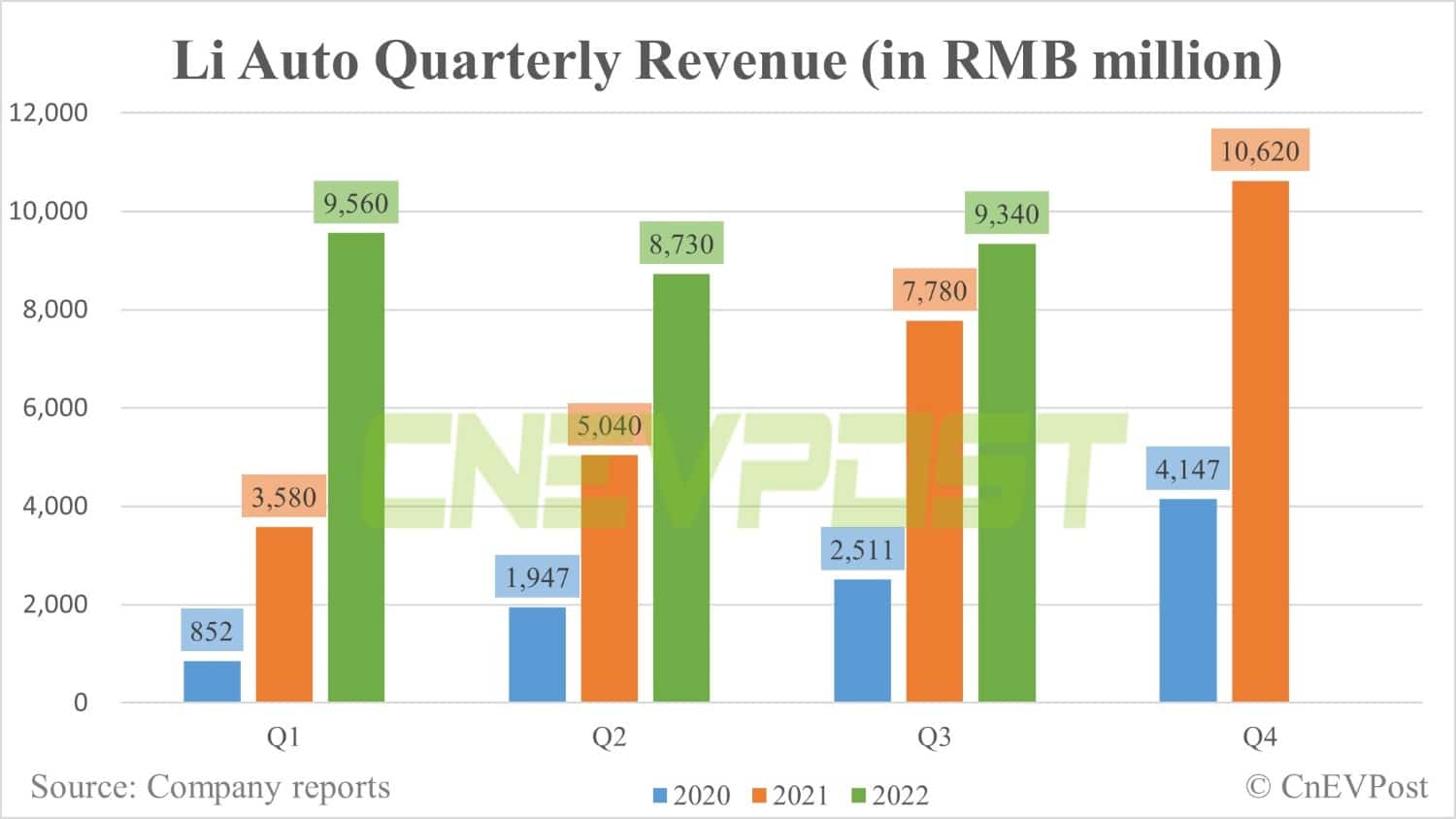

The company gave fourth-quarter revenue guidance of RMB 16.51 billion to RMB 17.61 billion when it announced its third-quarter earnings.

Fourth-quarter earnings

Yu's team said Li Auto is expected to report solid results for the fourth quarter, with margins likely to rise and auto margins recovering to around 21 percent.

The team expects Li Auto to report revenue of RMB 18 billion, gross margin of 21.1 percent and adjusted earnings per share of 0.45 in the fourth quarter.

This compares to the current consensus analyst estimates of RMB 17.6 billion, 21.6 percent, and 0.37, respectively, in a Bloomberg survey.

Li Auto reported revenue of RMB 9.34 billion in the third quarter, with a gross margin of 12.7 percent. The gross margin was a new low since the first quarter of 2020, as Li ONE's accelerated phase-out hurt margins.

Yu's team said their model assumes a significant increase in operating costs relative to the third quarter.

To outperform competitors in first quarter

Yu's team believes that Li Auto management's delivery guidance for the first quarter will be to target more than 50,000 units, including deliveries of the Li L7 five-seat SUV, which will begin next month.

Li Auto delivered 15,141 vehicles in January, down 28.69 percent from 21,233 in December but up 23.42 percent from 12,268 in the same month last year, data released earlier this month showed.

In contrast to Nio, Li Auto has managed the launch of its latest models, the Li L8 and Li L9, very effectively in recent months, capturing the initial wave of demand, according to Yu's team.

This is important in a highly competitive market driven by product cycles, i.e., reducing the risk of customers waiting too long for a new vehicle and cancelling their pre-orders, the team noted.

"Our channel checks point to an order book of around 20,000 for the L7. In respect to gross margin, 1Q should see further improvement to >21.5% and be profitable on a non-GAAP basis (excluding SBC)," the team wrote.

All of Li Auto's current models are extended-range electric vehicles (EREVs), essentially plug-in hybrid vehicles (PHEVs), targeting a larger market.

Test will come in second half of the year

Yu's team believes the true test for Li Auto will come in the second half of the year, when it will strive to maintain demand momentum with its three relatively large EREV SUVs as competition intensifies.

Battery electric vehicles (BEVs) will make only a small contribution to Li Auto's sales in 2023, with the smaller Li L6 SUV expected to launch in 2024, the team noted.

The team sees some natural cannibalization of the Li L7 and Li L8, though this could be offset by it taking more shares from the German luxury carmaker's gasoline models.

The premium segment has been slower than anticipated to fully electrify but that will certainly change over time, the team said.

Later this year, there may be growing concerns about cannibalization, especially as more BEV competition hits the market and battery costs normalize, Yu's team said.

For the full year, the team expects Li Auto to sell 250,000 vehicles, which would result in sales of RMB 90 billion, but below CEO Li Xiang's "aspirational" RMB 100 billion target.

Gross margins should also improve as the production of new models reaches a steady run rate, likely at 22.5 percent in 2023, according to the team.

"Positioning wise, Li Auto remains the favorite in the group and likely stays there unless evidence of softening demand emerges or execution slips," the team wrote.