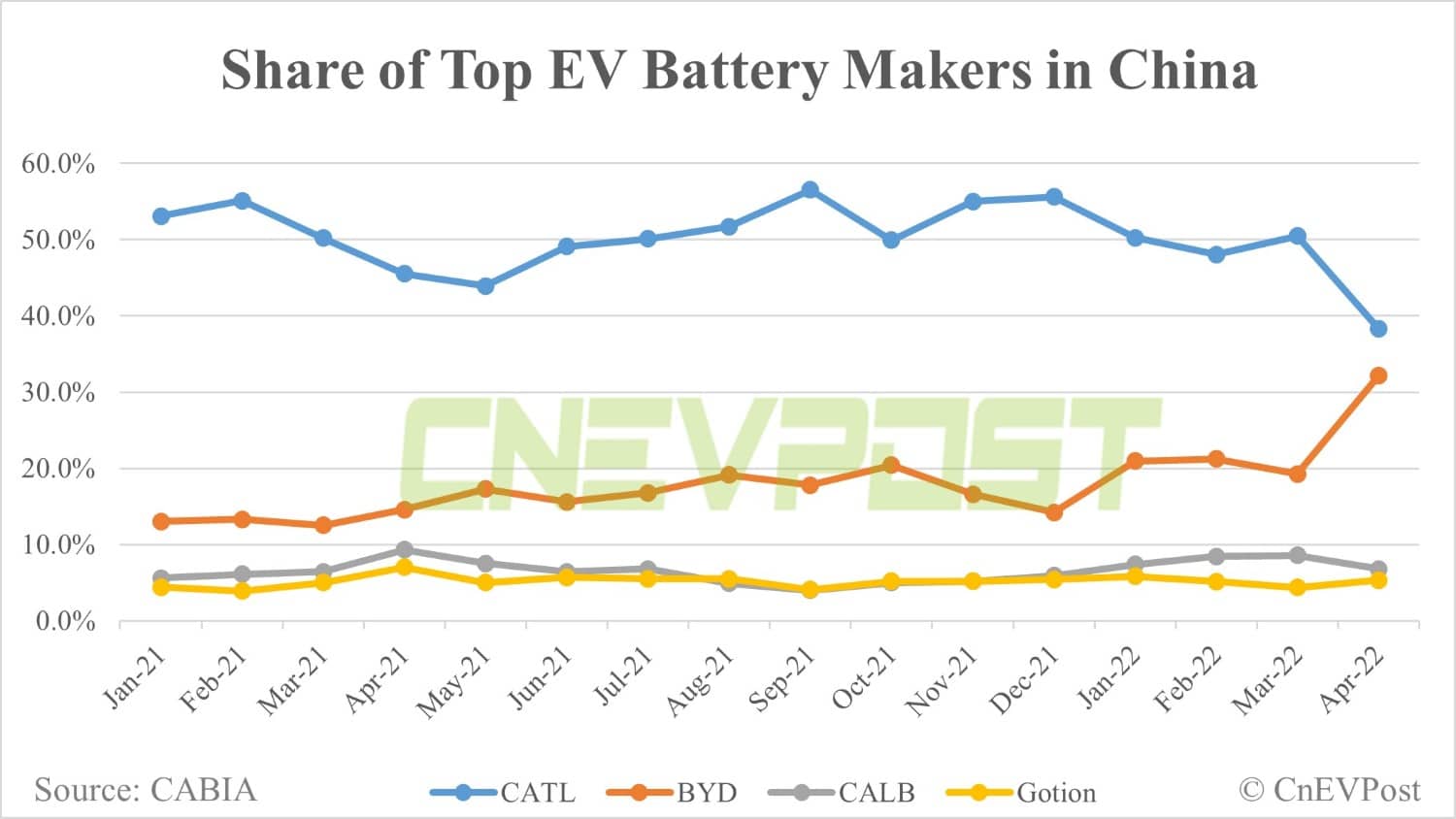

BYD's share reached 32.2 percent in April, narrowing the gap to 6.1 percentage points from CATL's 38.3 percent share.

Contemporary Amperex Technology Co Ltd (CATL, SHE: 300750) has been the absolute leader in China's power battery market, but that advantage narrowed significantly in April as Covid led to severe production disruptions for its customers.

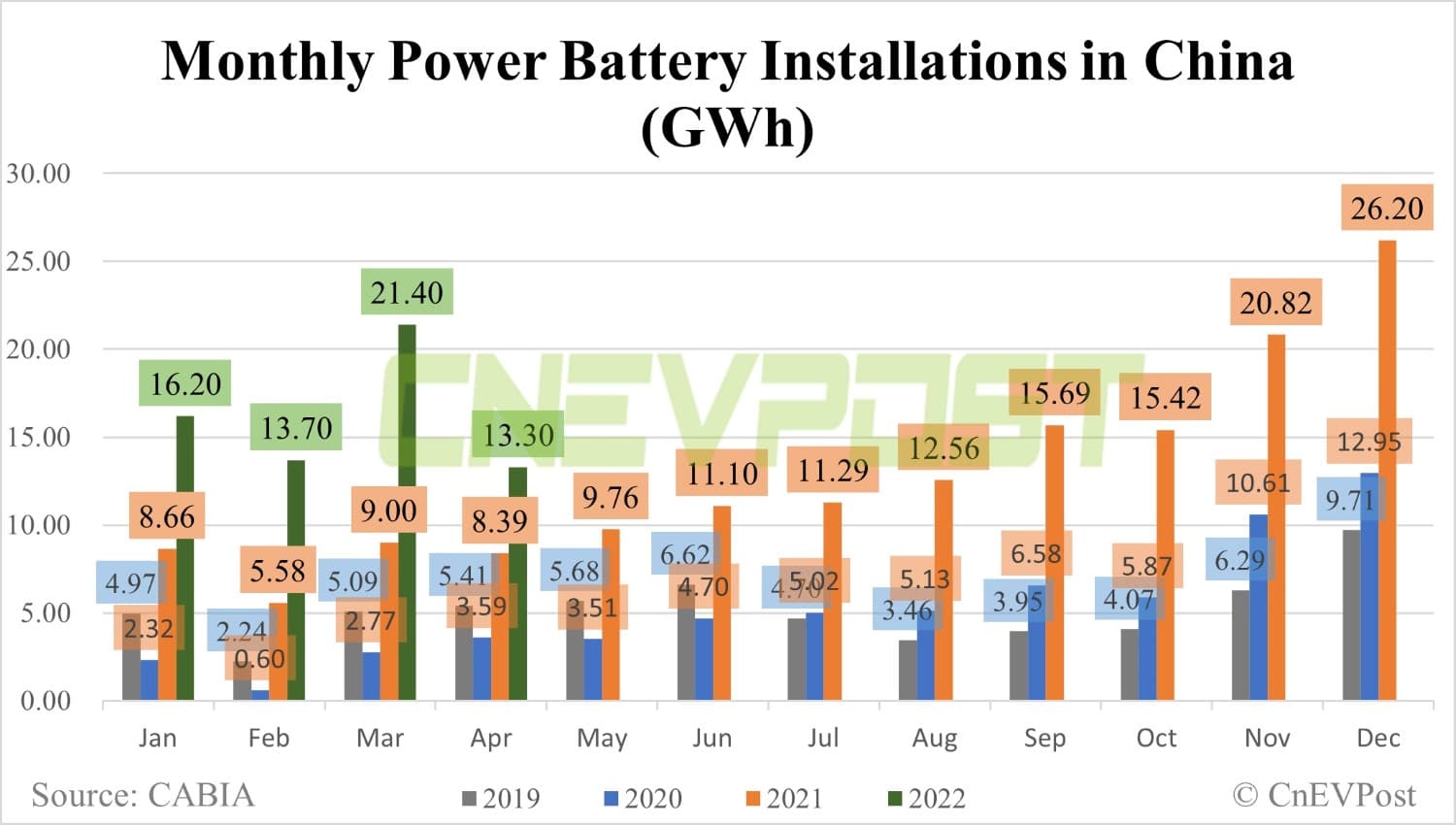

In April, China's power battery installed base was 13.3 GWh, up 58.1 percent year-on-year, but down 38.0 percent from March, according to data released today by the China Automotive Battery Innovation Alliance (CABIA).

CATL's installed base in April was 5.08 GWh, with a 38.3 percent market share, still ranking first, but down 12.2 percentage points from March's 50.5 percent.

BYD's (OTCMKTS: BYDDY, HKEX: 1211) installed base in April was 4.27 GWh, with a market share of 32.2 percent, ranking second, up 13 percentage points from 19.2 percent in March.

This narrowed the gap between BYD and CATL in China's power battery market share to 6.1 percentage points, the lowest since CABIA data became available.

Behind this development is a divergence in the performance of the two's battery customers in NEV sales in April.

CATL's major customers include Tesla (NASDAQ: TSLA), Nio (NYSE: NIO, HKEX: 9866), Xpeng Motors (NYSE: XPEV, HKEX: 9868), and Li Auto (NASDAQ: LI, HKEX: 2015), whose production and deliveries all plunged in April.

Tesla China produced 10,757 vehicles in April, with wholesale sales of 1,512 units, according to data released yesterday by the China Passenger Car Association (CPCA).

Compared to the 65,814 wholesale sales in March, Tesla's China-made vehicles decreased by 64,302, or 97.7 percent, in April.

Nio delivered 5,074 vehicles in April, down 49 percent from March. Xpeng delivered 9,002 vehicles, down 42 percent from March. Li Auto delivered 4,167 vehicles, down 62 percent from March.

BYD's power cells are mainly used in the company's own models, although it also supplies batteries for models including Ford's Mustang Mach-E.

For comparison, BYD sold 106,042 NEVs in April, up 1 percent from March and up 313 percent from a year ago.

This is the second consecutive month that BYD has sold more than 100,000 NEVs after selling 104,878 units in March, another record high.

Notably, BYD is a major player in the lithium iron phosphate (LFP) battery market, ranking first with 4.19 GWh of such batteries installed in April, with a share of 47.14.

CATL ranked second with an installed base of 3.05 GWh and a share of 34.29 in April.

In the ternary Li-ion battery market, CATL still holds the absolute leading position, with 2.03 GWh installed in April and a share of 46.56 percent.

BYD's ternary lithium battery installed volume in April was only 0.08 GWh, with a share of 1.84 percent.