Li Auto reported strong fourth-quarter results and provided a better-than-expected outlook for first-quarter sales, Deutsche Bank said.

Li Auto (NASDAQ: LI) reported its fourth quarter 2023 financial results today. As usual, Deutsche Bank analyst Edison Yu's team shared their first look at the results.

Here's what the team said in a research note sent to investors today.

Li Auto delivered strong 4Q23 results and provided a better than expected 1Q24 volume outlook.

Deliveries were already reported for 4Q at 131,805 units, leading to revenue of 41.7bn RMB, slightly above our forecast of 41.0bn due to higher ASP (306k RMB vs. DBe 301k).

Total gross margin of 23.5% beat our/consensus estimates of 21.0%/21.7%, on stronger vehicle margin of 22.7% (+150bps QoQ), boosted by true-up of warranty reserve.

Services margin of 45.5% was consistent with our model. Opex of 6.8bn was above our expectation, driven by higher spending on both SG&A and R&D.

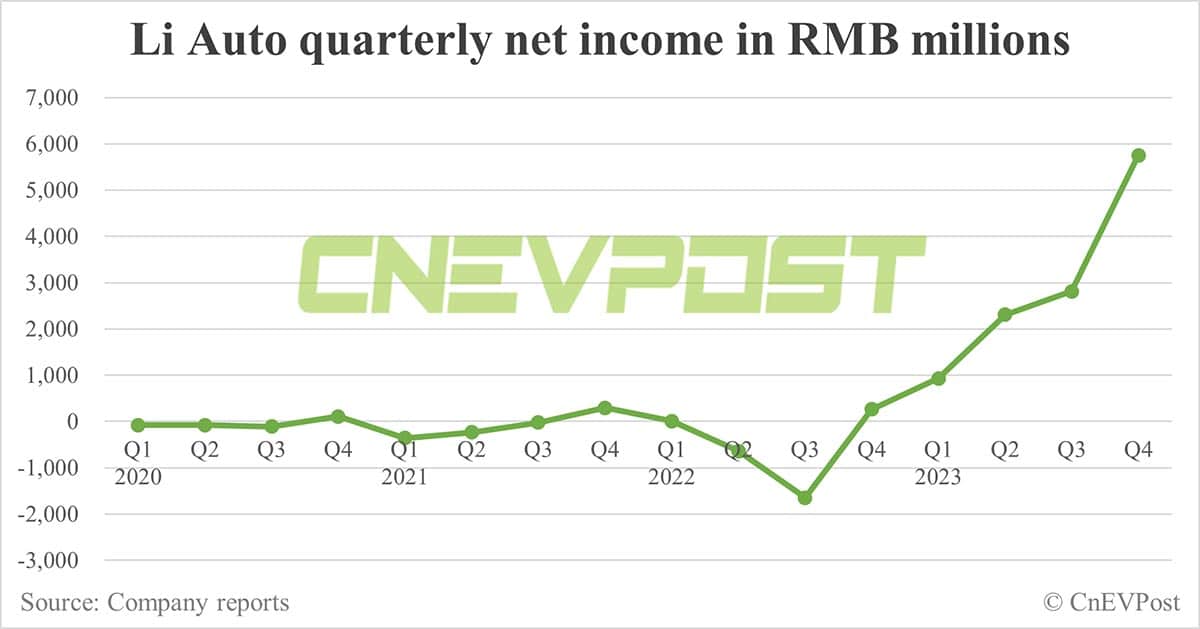

Adjusted EPS was 4.23, easily beating DBe/ consensus of 3.08/2.75. Free cash flow came in at >14bn, materially better than anticipated, supported again by working capital. See Figure 1 for details.

Management provided strong 1Q guidance calling for 100,000-103,000 in deliveries, higher than our 95,000 forecast, assuming a big step-up in March to +50,000 units vs. Jan at only 31,165.

Revenue is expected to be 31.25-32.19bn RMB in 1Q, implying lower ASP sequentially (likely dragged down by promotional activity); gross margin is expected to be around 20%.

Looking ahead, Li Auto is targeting +70,000 units in June and 100,000 units (per month) exiting the year.