"Even if we embed some degree of conservatism, this suggests further demand deterioration in Aug/Sep on a sequential basis."

Xpeng Motors on Tuesday reported second-quarter revenue that beat expectations but gave yet another discouraging guidance for the next quarter.

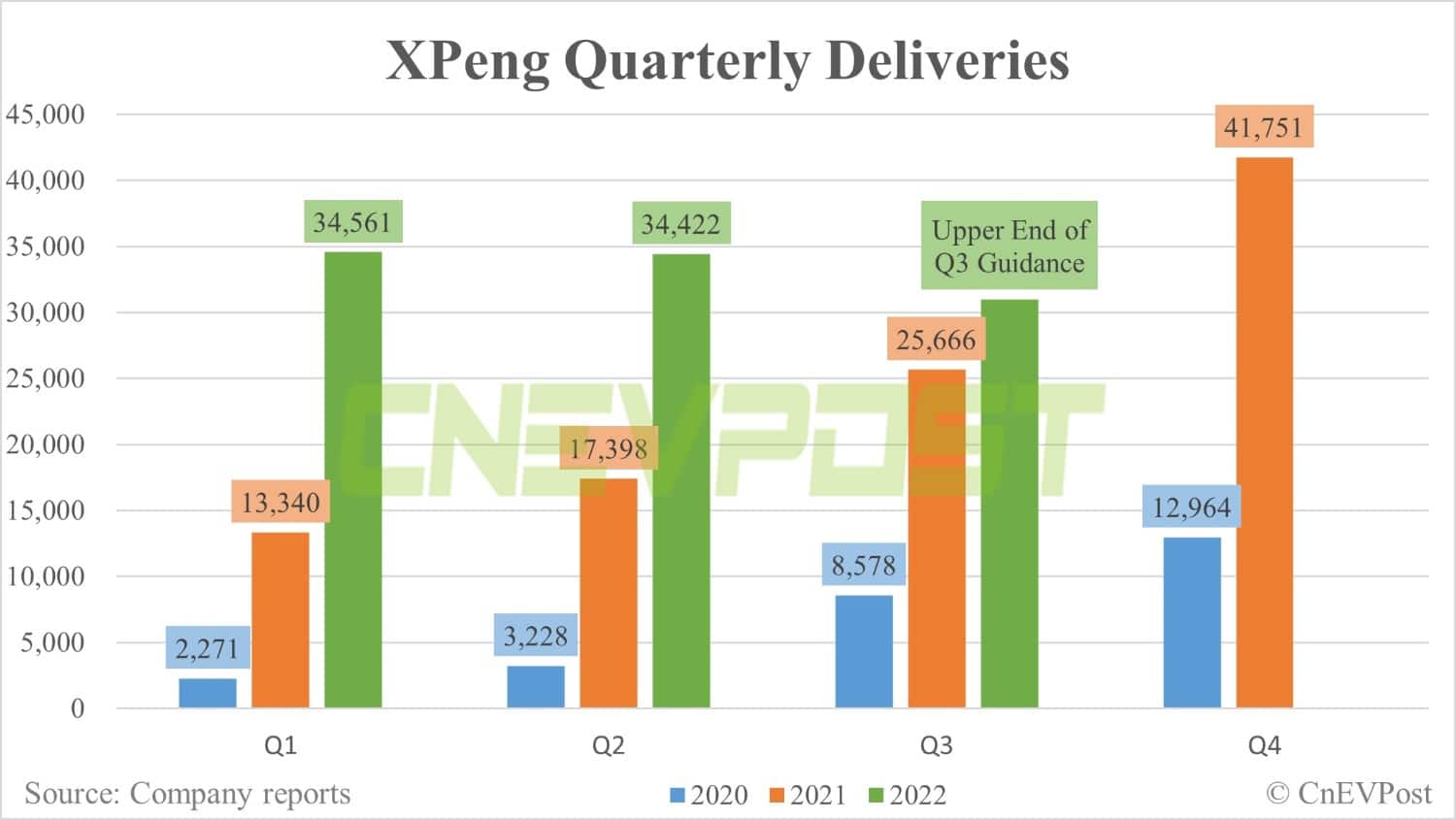

The company guided for third-quarter deliveries of 29,000 to 31,000 units, below consensus estimates of 36,000, Deutsche Bank analyst Edison Yu said in a research note sent to investors on Tuesday.

"Even if we embed some degree of conservatism, this suggests further demand deterioration in Aug/Sep on a sequential basis," the note reads.

This is largely due to greater than expected competitive pressure and deemphasis on lower-margin products, including Xpeng P5 and G3, Yu said.

Here are Yu's first look of Xpeng's second-quarter earnings report:

Xpeng delivered better than expected 2Q results but provided a very weak 3Q outlook, even worse than we previewed.

Deliveries for 2Q were already reported at 34,422 units, leading to revenue of 7.4bn RMB, in line with our forecast.

Total gross margin declined just 130bps QoQ to 10.9%, beating our 9.2% estimate (consensus 9.6%), driven by higher vehicle margin. We suspect battery input costs proved to be less of a drag than anticipated.

Opex of 2,929m RMB essentially matched our model.

All together, EPS of (2.88) came in worse than our (2.23) forecast due to a large FX revaluation loss.

Management provided very weak 3Q volume guidance, calling for only 29,000- 31,000 deliveries, vs. our below consensus 36,000 forecast (translating into 6.8- 7.2bn RMB in revenue).

Even if we embed some degree of conservatism, this suggests further demand deterioration in Aug/Sep on a sequential basis.

We attribute this mainly to greater-than-expected competitive pressure and deemphasis on lower margin products (P5/G3).

Xpeng began offering promotions in July as the order book was softening, suggesting to us the previous price hikes may have been too aggressive.

We don't see a major recovery until 4Q with the launch of the G9 SUV which we think could sell at least 10,000 units (mostly in Nov/Dec) and deliver superior margins.

On gross margin, management expects 3Q to show improvement QoQ as a full period of price hike net of promotional activity should still be a benefit; P7 mix should also improve.

For 2023, management continues to plan to launch a smaller B-class SUV (in first half; possibly called G5) on the next-gen platform, similar to Model Y which we think could become the company's highest volume model.

There will be another new larger C-class vehicle that will garner lower volumes. And also the P7 sedan will get a refresh with lidar option and other improvements.