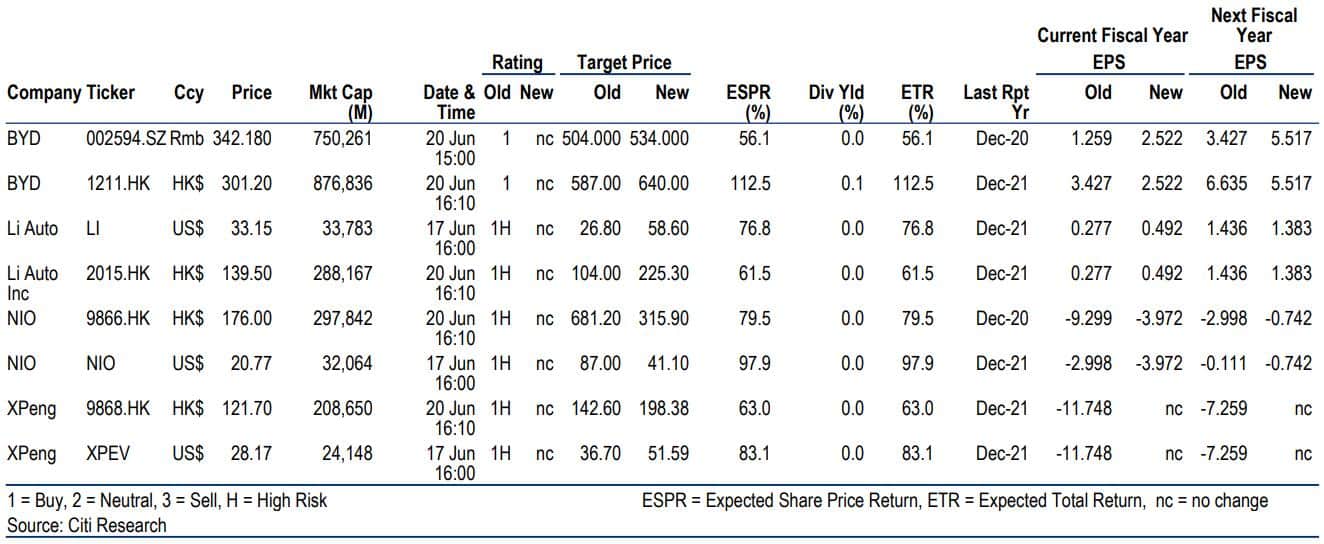

Citi lowered its price target on Nio to $41.1 from $87 and raised its price targets on BYD, Xpeng, and Li Auto, continuing to name Nio and BYD as top picks.

(Image credit: CnEVPost)

As nearly all Wall Street analysts have continued to cut their price targets on Nio (NYSE: NIO, HKG: 9866, SGX: Nio) over the past year as the stock sinks, one has maintained restraint.

Citi analyst Jeff Chung has maintained his $87 price target on Nio since last November, becoming an outlier and moving further and further away from the market consensus.

On Tuesday, the analyst's team finally adjusted its price target on Nio, but it was not because they were pessimistic about the electric vehicle (EV) maker's prospects, but because they adjusted their approach to valuing China's EV industry.

Chung's team highlighted that their top picks in the Chinese EV sector remain BYD (SHE: 002594, HKG: 1211, OTCMKTS: BYDDY) and Nio, followed by Li Auto (NASDAQ: LI, HKG: 2015) and Xpeng Motors (NYSE: XPEV, HKG: 9868).

In short, the team previously valued the Chinese EV sector based on P/S (price-to-sales), using revenue as a benchmark for valuation.

But with things changing rapidly, the team now believes a more reasonable approach would be based on PEG (price/earnings-to-growth), making revenue per share and expected growth rate more important.

In a research note sent to investors Monday, Chung's team explained why the change was made:

In a unique analysis of the full lifecycle (FL) costs of vehicle ownership in China, we present two key non-consensus conclusions:

(1) NEV buying decisions increasingly hinge on the attractive value proposition of FLC costs vs. NEV interior space, a factor that we see as overlooked by capital markets; and

(2) In a scenario of both gasoline & lithium-carbonate prices shooting up by another 25%-50% YoY into 23E, FL ownership costs would be 36% lower for NEVs than for ICEs.

Feeding these findings into our models, we raise our volume forecasts for China’s leading NEV makers, and in turn our 22-25E/30E China NEV penetration rates.

In our view, the market will gradually switch from valuing NEV makers on P/S to using PEG (& PER); on this basis we lift our TPs BYD/Li/Xpeng, and expect 98% total return for Nio.

Based on this changed valuation methodology, Citi now has a $41.1 price target on Nio's US-traded ADRs, less than half of its previous $87 target, but implying an upside of about 98 percent from Friday's closing price. The US stock market was not trading on Monday due to a holiday.

Battery electric vehicle models will take market share in A-segment SUVs and B/C-segment sedans going forward, the team said, citing their full lifecycle cost analysis.

Among specific car models, Nio’s ET5 offers larger space at a lower full lifecycle cost versus Tesla Model 3, and the newly released ES7 also shows competitiveness with larger-space cars, the team said.

Here is how they now value Nio:

The company’s current market cap is Rmb209bn. With our new 24E NP forecast at Rmb3.8bn, and our expectation of around 50% 24-26E EPS CAGR, this suggests the stock is now trading at 55x 24E PER with around 1.1x PEG.

By assigning similar PEG in line with Tesla and BYD at 2.2x over 24-26E growth, we expect the stock still offers 100% upside with an implied 24E PER of 110x. We set our new TP at US$41.1 (from US$87.0), which implies 2023/24E PS multiples of 2.4x.

Similarly, based on the new valuation methodology, Citi now has a $51.59 price target on Xpeng's US-traded ADRs, up from $36.7 previously and implying an upside of about 83 percent from last Friday's close.

Their latest price target on Li Auto is $58.6, up from $26.8 previously, implying an upside of about 77 percent from last Friday's close.

The team's latest price target on BYD's Hong Kong-traded stock is $640, up from $587 previously, implying 112 percent upside from Monday's close.

Citi maintained its Buy rating on all four companies.