Edison Yu's team lowered their price target on Li Auto by $6 to $28, based on 3.0x 2023E EV/Sales, down from 3.5x previously.

Deutsche Bank cut its price target on Li Auto (NASDAQ: LI, HKG: 2015) ahead of the company's first-quarter earnings report due next Tuesday.

Analyst Edison Yu's team lowered their price target on Li Auto by $6 to $28 based on 3.0x 2023E EV/Sales, down from 3.5x previously, in a research note sent to investors today. The team maintains a Hold rating on the company.

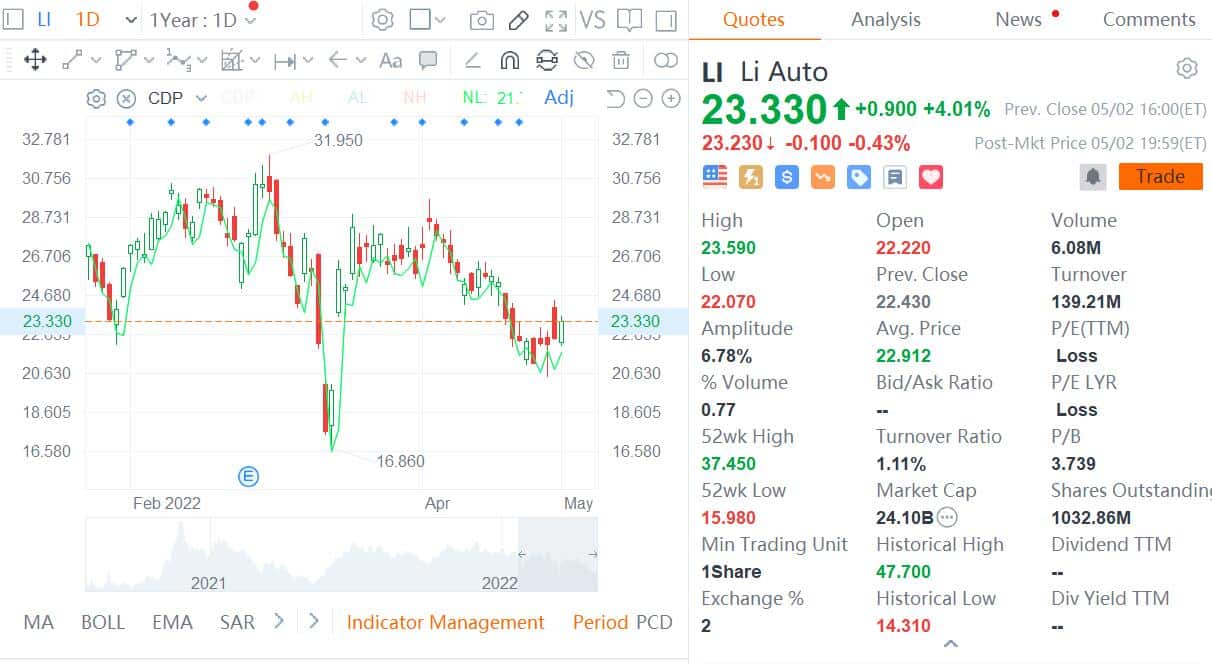

Shares of Li Auto traded in the US closed up 4.01 percent to $23.33 on Monday, and the price target implies a 20 percent upside.

First-quarter earnings preview

Li Auto will report unaudited first-quarter earnings on Tuesday, May 10, before the US stock market opens, the company said on April 26.

The company has already released data showing it delivered 31,716 vehicles in the first quarter, which is near the upper end of its guidance range of 30,000-32,000 vehicles.

It previously guided for first-quarter revenue of RMB 8.84 billion-9.43 billion, implying year-on-year growth of 147.2-163.7 percent.

Yu's team expects Li Auto to have a mostly in-line quarter, with revenue of RMB 9.6 billion, gross margin of 21.1 percent and adjusted earnings per share of 0.05.

This compares with the consensus of analysts in the Bloomberg survey of RMB 9.67 billion, 21.2 percent, and 0.07.

Li Auto's margins will be negatively impacted by inflationary pressures, Yu's team noted.

Second quarter and 2022 outlook

Li Auto's sole model, the Li ONE, delivered 4,167 units in April, down 62 percent from 11,034 in March and 25 percent from 5,539 in the same month last year, according to data released May 1.

Yu's team believes the company will see material monthly improvement in sales in May and June and expects it will give guidance of 22,000-24,000 vehicles for second-quarter deliveries.

However, the team also noted that visibility is quite low given the supply chain situation and near-term developments will still need to be closely monitored in the coming weeks.

Yu's team's base case assumes that Li Auto's production returns to a more normal level in the second half of the year.

The company has about 16,000 units/month of capacity at its Changzhou plant, but may not reach that level until the fourth quarter, according to the team.

In addition, deliveries of the new L9 full-size EREV SUV are still scheduled to begin in the third quarter, probably by the end of the quarter, at a capacity of between 5,000-10,000 units/month, Yu's team noted.

(Li Auto L9. Image credit: Li Auto)

Overall, the team lowered their full-year delivery forecast for Li Auto from 175,000 to 150,000 units to account for the negative impact of Covid lockdowns and incremental supply chain constraints.

However, the team increased gross margin by 50 basis points to 22.3 percent, reflecting the price increase for the Li ONE and the higher price point for the upcoming L9.

Tactically, Yu's team does not see compelling reasons to be incrementally bullish as questions may arise about how resilient Li Auto's operational execution will be going forward.

The team believes Li Auto's new pure-play electric vehicle next year will be a headwind for gross margins, especially if raw material prices continue to be high and it must accelerate operating expenses as well as capital expenditures to build out its new production line, charging infrastructure network and higher levels of ADAS capability.

In addition, the L9 SUV targets a market that includes the Toyota Land Cruiser and Range Rover, which is a relatively small segment, the team noted.