Deutsche Bank analyst Edison Yu's team lowered their price target on Nio from $70 to $50, maintaining a Buy rating.

Nio (NYSE: NIO, HKEX: 9866) will report unaudited fourth-quarter and full-year 2021 results on Thursday, March 24, after the US stock market closes (March 25 morning Beijing Time). What should investors look for? Deutsche Bank analyst Edison Yu's team offered their take.

"We expect a mostly in-line quarter and somewhat soft 1Q22 guidance, where we think management could guide for 25,000 in vehicle deliveries (flat QoQ)," the team said in a research note sent to investors on Sunday.

Previously released data showed Nio delivered a record 25,034 vehicles in the fourth quarter, near the upper end of its guidance range for fourth-quarter deliveries of 23,500 to 25,500.

Nio's previous guidance for fourth-quarter revenue was RMB 9.38 billion to RMB 10.11 billion, representing growth of about 41.2 percent to 52.2 percent over the same period in 2020.

Yu's team expects Nio to report revenue of RMB 9.72 billion and adjusted EPS of RMB -0.86 in the fourth quarter. They expect the gross margin to be 17.0 percent, down 3.3 percentage points from the third quarter due to the timing of regulatory credits.

As a comparison, the Wall Street consensus estimate is RMB 9.74 billion, RMB -1.11 and 17.4 percent, the team notes.

For first-quarter guidance, the team believes Nio's management may guide for about 25,000 deliveries, implying March deliveries of about 9,500 units, including a small number of ET7 sedans.

That factors in the Shenzhen Covid lockdown limiting deliveries, and the Shanghai impact has been minimal thus far, the team noted.

"Based on our channel checks, we don't anticipate the lockdowns being overly harmful to EV production as the local governments are handling the issues pretty effectively and creative solutions are being implemented to keep plants open," the report reads.

Outlook for 2022

In their note, Yu's team also provided their outlook for Nio in 2022, saying this will be a pivotal year both strategically and financially.

According to Nio's previously announced plans, it will deliver three new models based on the NT2.0 platform this year - the ET7, ET5 and ES7 - with the first delivery of the ET7 set to begin on March 28.

Yu's team estimates that the ET7 has received at least 60,000 pre-orders and says the model has earned good reviews based on local media reports.

The team also provided their outlook for Nio's deliveries this year:

On a monthly basis, Nio has essentially been stuck at a peak of 10,000-11,000 deliveries since September. This will change in 2Q where we see the run-rate increasing to 15,000-20,000/month by June.

Then in 2H, Nio's 2nd plant NEO Park will come online, producing the ET5 mid-size sedan and ES7 SUV. Assuming both take a few months to ramp-up and cannibalize some portion of existing first-gen SUV sales, we think the monthly run-rate could reach 25,000/ month in December (and then increase further to 30,000 in 1H23).

Overall, we raise our deliveries forecast from 160,000 to 167,000, with potential upside should new models ramp faster/earlier than anticipated.

In terms of gross margin, Yu's team expects rising raw material prices, especially lithium carbonate, to have a negative impact, but its new 75-kWh hybrid LFP pack will help offset some of that by bringing down raw material bills by several thousand RMB.

Higher nickel prices could also be a potential headwind, but will be highly dependent on the dynamics of the contract, the team said.

"We lower our overall gross margin by 50bps to 19.2% (implies around flattish YoY). Opex will likely to see a material step up across R&D and SG&A as it further develops ADAS/AD tech and rapidly expands infrastructure," the team wrote.

Lowered Nio price target by $20 to $50

The team maintained its Buy rating on Nio, but lowered its 12-month price target on Nio to $50, down 28.6 percent from the previous $70, due to lower valuation multiples.

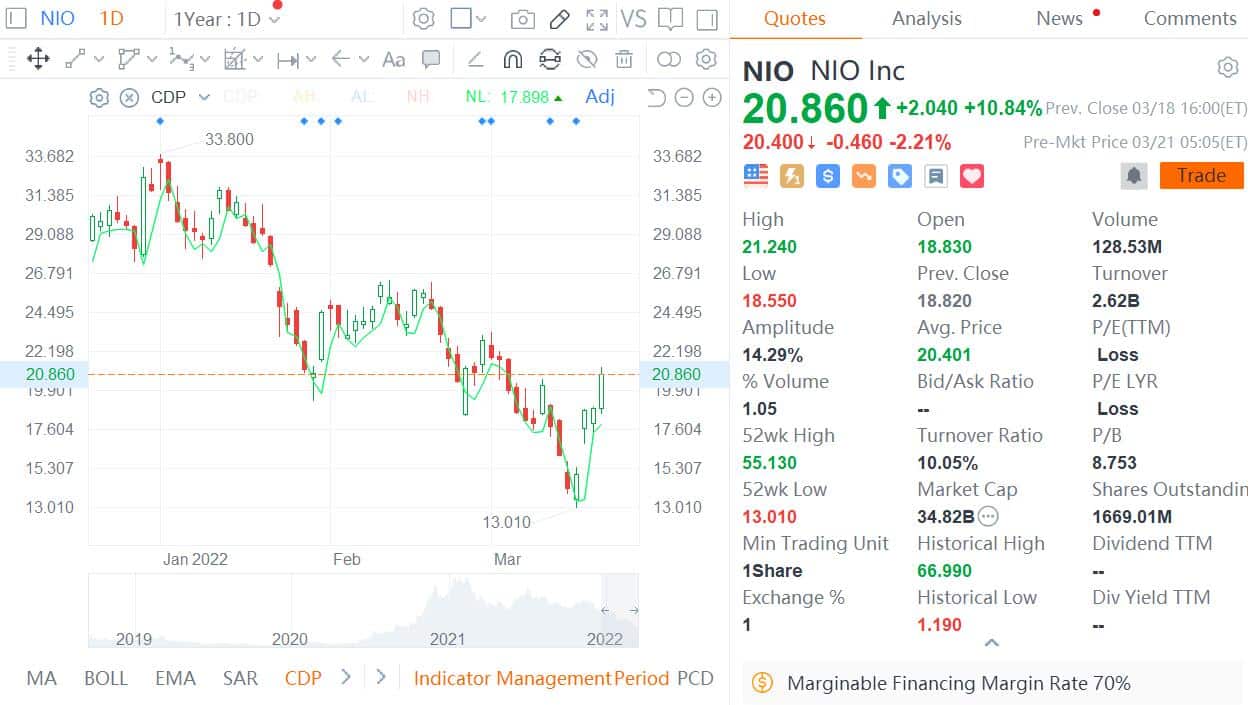

Nio closed up 10.84 percent to $20.86 in the US on Friday. The target price implies an upside of about 140 percent.

Here is how the team explains this adjustment in detail:

Looking ahead, we can envision the stock being choppy until late 2Q when ET7 deliveries start picking up, paving the way for the stock to outperform for the rest of the year on a relative basis.

We think the narrative of going from 10k/month in deliveries to 25k/month exiting the year can alleviate many investor concerns about demand and supply chain management.

We lower our price target by $20 to $50, based on 5.0x 2023E EV/Sales or 40-50% discount to US comps such as TSLA/LCID (vs. prior 8.0x), to account for the derating in Chinese ADRs following concerns about delisting/geopolitical risks, but reiterate our Buy rating, seeing significant long-term upside once the shareholder base stabilizes and Nio gets credit for its upcoming product cycle inflection.

The main risks for Nio are supply chain constraints and regulatory scrutiny.

Demand for EV components are very high as adoption increases causing supplier shortages for chips and battery cells. This could limit Nio's sales growth and force customers to wait longer for delivery.

Separately, US regulators have stepped up scrutiny of Chinese companies listed on US exchanges, with potential actions to de-list them if certain agreements are not settled upon with the Chinese government.