CICC on Tuesday initiated coverage on Li Auto's H-shares with an Outperform rating and a target price of HK$187, corresponding to 6.5x EV/Revenue by 2022.

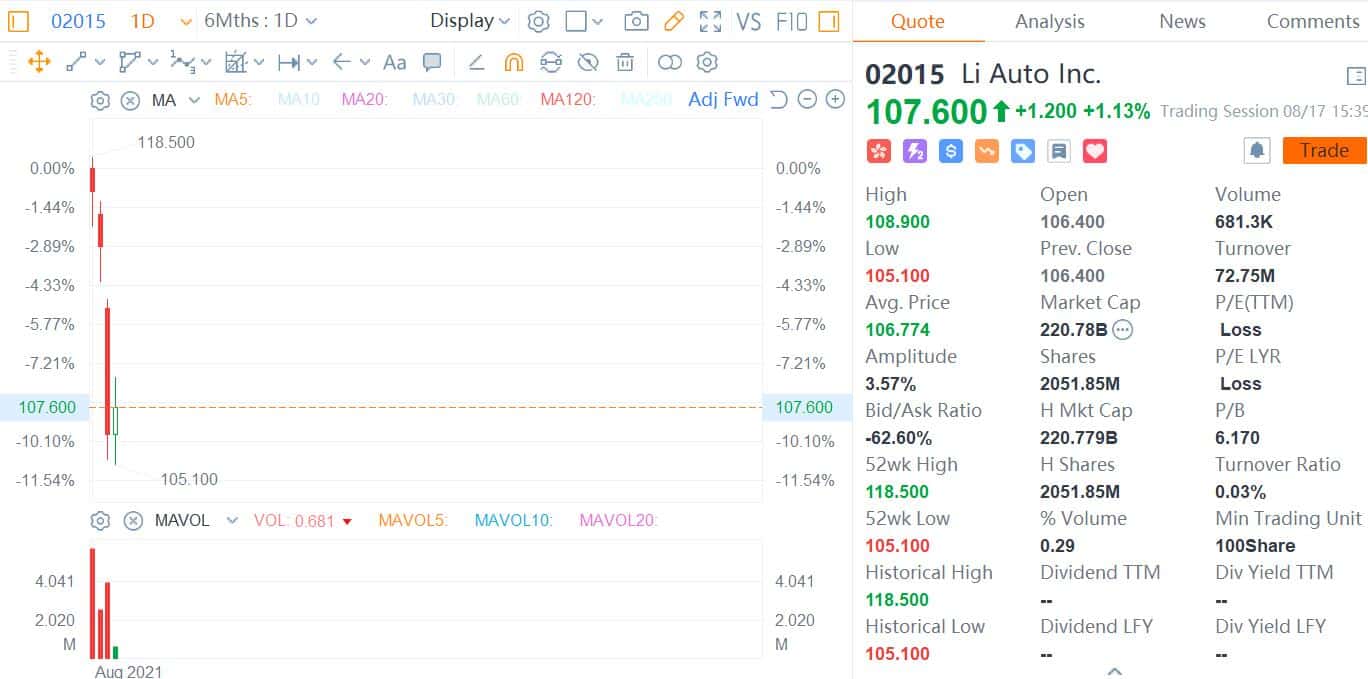

Li Auto closed at HK$ 106.4 in Hong Kong on Monday, and CICC's price target implies 76 percent upside.

The report maintains an Outperform rating on Li Auto's US shares, with a 7 percent price target increase to $48, implying 67 percent upside, due to higher medium- to long-term sales expectations.

Currently, Li Auto's valuation corresponds to 3.9x 2022 EV Revenue, and the analysts expect the company's EPS to be RMB -0.44, -0.35 and 0.74 in 2020, 2021 and 2022, respectively.

The report said Li Auto took delivery of its first model, the Li ONE, in late 2019 and that sales of the model have continued to climb in popularity since then.

The analysts attribute the success of the Li ONE to the company's deep understanding of consumer needs and strong product definition, design and execution capabilities.

Li Auto's "unified configuration" strategy is unique in the industry and not only reduces costs, but also gives all users the same quality experience, the report said.

According to the analysts, Li ONE's success is no coincidence; the company has turned its insight into consumer needs and its ability to polish its products into a "strong product gene".

With this gene, the success of Li Auto's first model can be replicated. The company's new models planned for next year are expected to be well-received across multiple market segments, the report said.

Pure electric models are the target for Li Auto, whose high-voltage pure-electric platforms, the Whale and the Shark, are set to launch in 2023.

The analysts believe Li Auto's full-stack self-driving platform, due in 2022, will further extend the company's advantage, making it a leader in the current round of smart electrification in the automotive industry.

The analysts say the biggest difference between their view and the market's is that while the company's late launch of pure electric models will not be an impediment to the company's turn, its subsequent launches are expected to narrow valuation differentials.

Potential catalysts include the full-stack self-driving system and new models, the report said.

Li Auto was up about 1 percent to HK$107.6 at press time. It is down about 9 percent since its Hong Kong listing.