While Li Auto's underlying execution remains strong, Nio, Xpeng will be more compelling growth stories in coming quarters, said Deutsche Bank.

Li Auto (NASDAQ: LI) reported strong second-quarter results yesterday, but shares fell sharply. Deutsche Bank analyst Edison Yu's team shared their thoughts on this.

"With expectations already quite elevated going into earnings, we are not overly surprised by the negative market reaction and continue to believe the stock is embedding a very positive trajectory, creating room to disappoint," the team said in an August 8 research note sent to investors.

Li Auto reported results yesterday that showed it saw record revenue of RMB 28.65 billion ($3.95 billion) in the second quarter, beating market expectations of RMB 27.25 billion. Its gross margin improved to 21.8 percent in the second quarter, up from 20.4 percent in the first quarter.

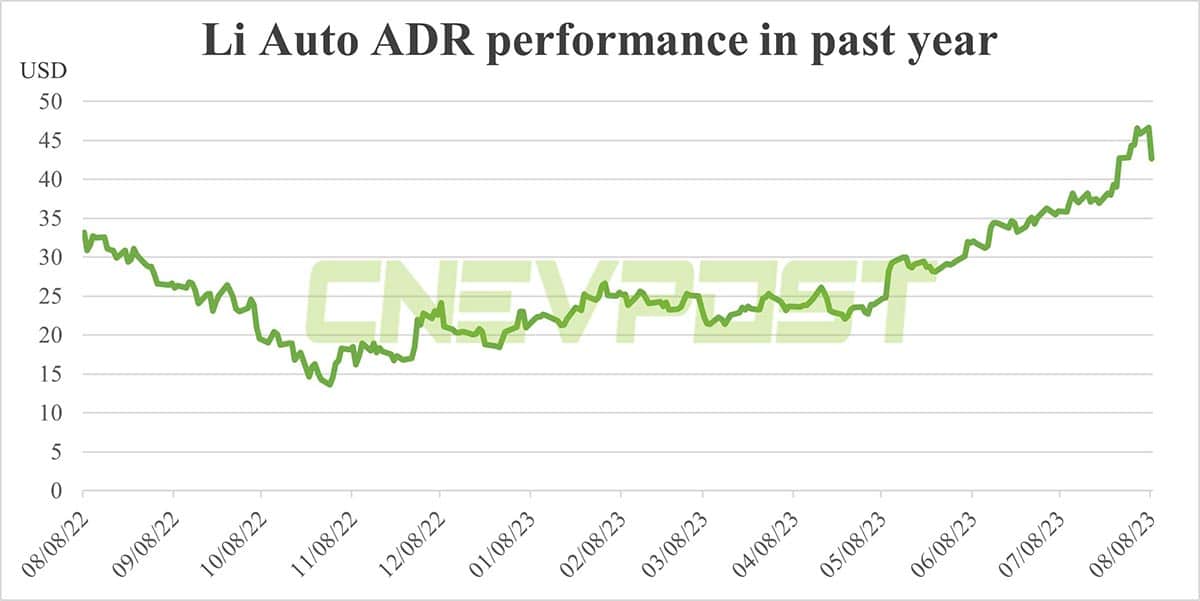

Nonetheless, the company's shares suffered a sell-off, dropping 8.62 percent to $42.63 by the close of US trading on Tuesday, the biggest one-day drop since January 6.

Incremental growth in Li Auto sales will likely be muted until the launch of the Li L6 next year, and there doesn't appear to be much upside in gross margins even with Li One fully phased out now, Yu's team said.

Additionally, battery electric vehicle (BEV) rollouts appear to be slow as pricing will be very high and naturally comes with new structural costs, such as building charging infrastructure, the team noted.

"While underlying execution remains strong, we believe Nio/XPEV have more compelling growth stories for the next few quarters and also benefit from strategic optionality," the team said.

Li Auto's first production model, the Li One, has been discontinued, and it currently sells the Li L7, Li L8, and Li L9, all extended-range electric vehicles (EREVs).

The company expects to launch its first BEV model, the Li Mega, within the year, aiming to make it the number one seller among models priced at more than RMB 500,000 yuan.

Li Auto guided for third-quarter deliveries of 100,000-103,000 units, which Yu's team said is largely in line with their current forecasts, implying a flattish trajectory after exceeding 34,000 units in July.

Li Auto's goal is to see monthly sales reach 40,000 units during the year, which Yu's team believes may be difficult to maintain as competition intensifies and market share reaches its natural ceiling.

"We think Nio's new ES6 and Xpeng's upcoming G9 refresh could limit further growth on L7/L8 given more competitive entry level pricing," the team wrote.

Li Auto's market share among premium SUVs has reached around 20 percent and may have reached its near-term ceiling, considering that even German luxury carmakers BMW, Mercedes-Benz, and Audi each have a share of around 20 percent in the segment in China, according to the team.

Li Auto's future incremental growth will have to come primarily from the cheaper Li L6 SUV and BEVs, which will initially be expensive and won't garner a lot of sales, the team said. Li Auto management said the company will launch three new BEV models next year.

For the full year 2023, Yu's team raised its delivery forecast by 5,000 units to 355,000. The team expects Li Auto to post revenue of RMB 117 billion this year, while maintaining a gross margin of around 22 percent.