Nio reported weak first-quarter underlying results but showed surprising Opex discipline to start the year and also presented a better-than-feared outlook for second-quarter sales, Edison Yu's team said.

Nio (NYSE: NIO) today reported weaker-than-expected first-quarter earnings, but emphasized on the analyst call that more prudent cash management will follow, as well as expressing confidence in delivering 20,000 vehicles per month in the coming months.

As usual, Deutsche Bank analyst Edison Yu's team provided their first impressions of the earnings report.

Here's what the team had to say.

1Q23 Earnings First Look

Nio reported soft underlying 1Q results, largely as previewed but showed surprising opex discipline to start the year, and also initiated a better than feared 2Q volume outlook.

Deliveries for the first quarter were already reported at 31,041 units, leading to revenue of 10.7bn RMB, vs. our/consensus 10.9bn/11.7bn forecasts, hurt by lower ASP.

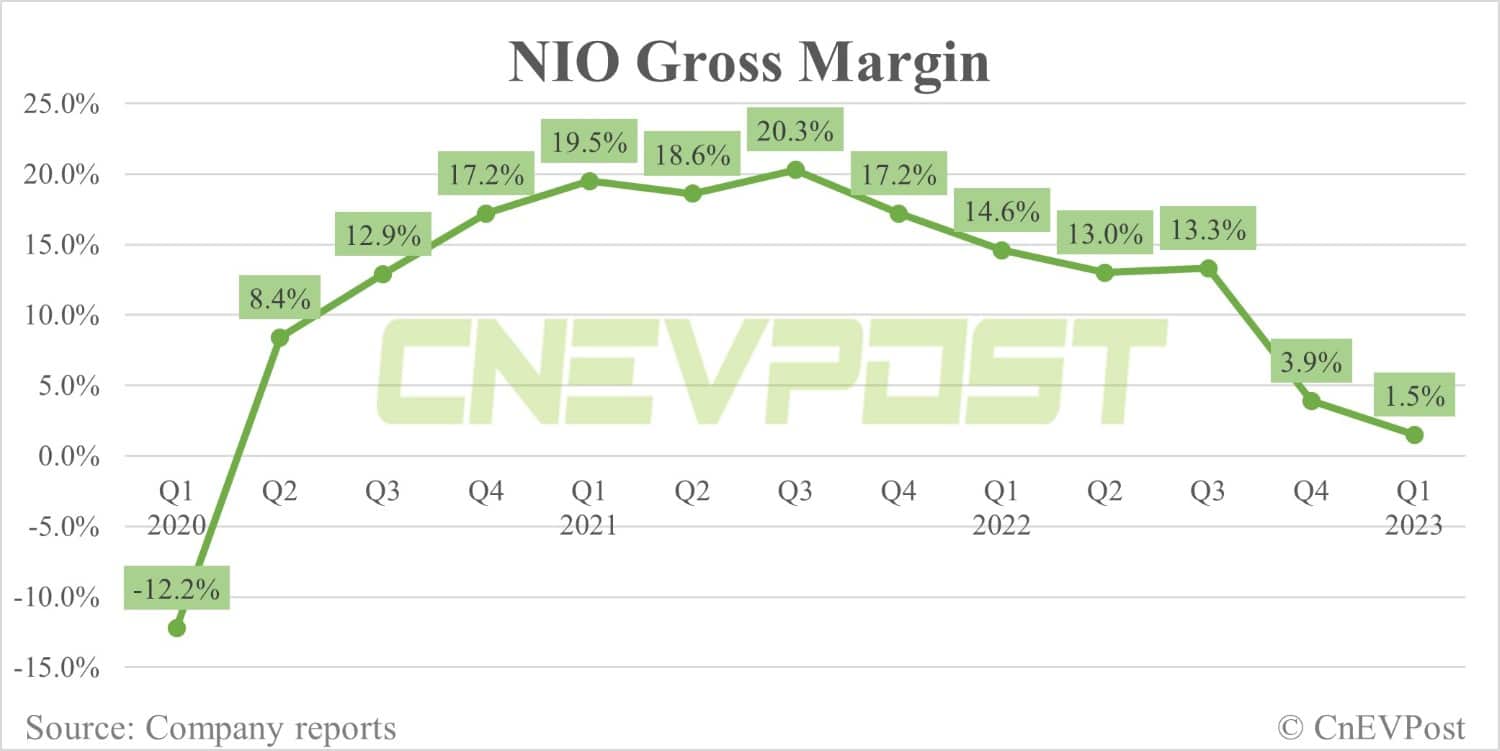

Gross margin of 1.5% was below our 2.5% forecast (consensus >7%), driven by downside in vehicle margin (5.1% vs. our 6.5%), partially offset by better "other" margin (-21.0% or +870bps QoQ).

Opex of 5.5bn was materially below our expectations, both on R&D and SG&A.

All together, adjusted EPS of (2.51) came in better than our/consensus estimates.

Management provided a stronger than expected outlook for 2Q23, calling for 23,000-25,000 deliveries. This compares to our 23,000 unit forecast and suggests June will be up materially QoQ (~11,000 at mid-point vs. just 6,155 in May) as the new ES6 ramps up quickly.

We suspect there were concerns June may see some supply chain constraints that don't appear to be materializing. This translates into 8.7-9.4bn RMB in revenue, vs. our 9.0bn forecast.

Looking beyond, management is targeting >20,000 deliveries per month in 2H including 10,000 of new ES6 in July. This will likely be difficult to achieve (sustain at least), in our view, given underperformance of the sedans (ET5, ET7) and we don't think management will get credit for this.

On vehicle margin, 2Q will still be under pressure with 3Q recovering back to double digits and 4Q >15%.

R&D is expected to still trend around 3-3.5bn (non-GAAP basis) per quarter and SG&A will step up sequentially in 2Q although the CEO's tone suggested certain incremental spend could potentially get pushed out at least until the performance of core Nio stabilizes.

Lastly, Nio is officially pushing out its operating profit breakeven target by a year (or less), which is long overdue based on our latest modeling.