Edison Yu's team continues to expect most automakers to be aggressive, as market share is a top priority.

China's major electric vehicle (EV) makers announced their April deliveries yesterday, and Deutsche Bank analyst Edison Yu's team provided their take, as usual.

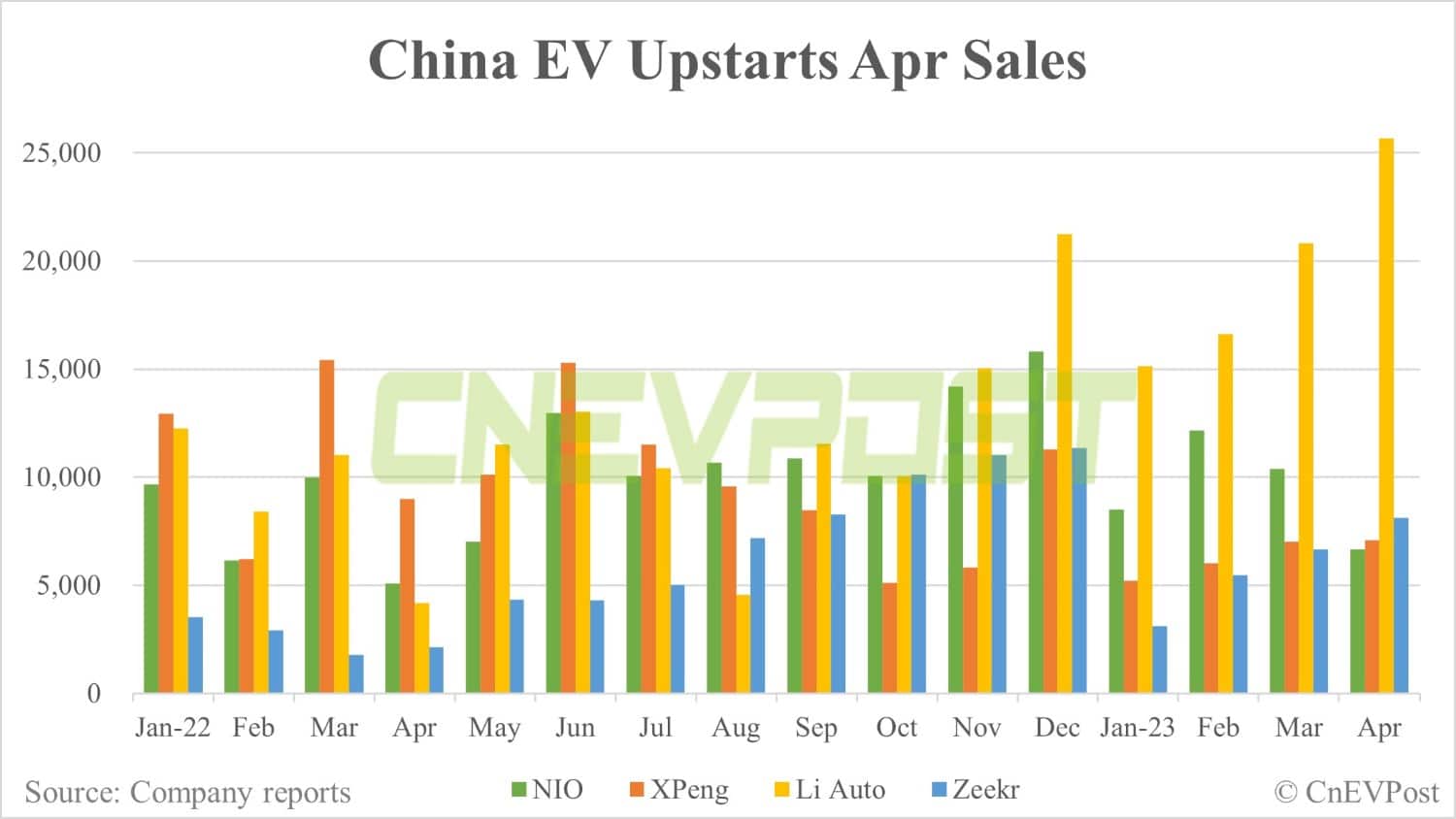

"April sales were generally better than feared for most OEMs we track with the exception of Nio who is struggling at the moment from both weak demand for its sedans and a major production platform transition for its SUVs," the team said in a note sent to investors yesterday.

Li Auto continues to impress, setting a monthly delivery record and showing continued strong traction for its three models in the premium SUV segment, the team said.

As a backdrop, Li Auto delivered a record 25,681 vehicles in April, surpassing the 20,000-delivery mark for the second consecutive month.

Nio deliveries fell further to 6,658 in April as the product switch continued. Xpeng delivered 7,079 vehicles in April, essentially unchanged from March, and the company appears to be on the cusp of emerging from the mire of weak sales that lasted about one year.

Here is the full text of Yu's team's note.

April sales were generally better than feared for most OEMs we track with the exception of Nio who is struggling at the moment from both weak demand for its sedans and a major production platform transition for its SUVs.

Li Auto continues to impress, setting a record for monthly deliveries, demonstrating continued robust traction in the premium SUV segment with its 3 models.

Xpeng's volume held in about flat MoM as new P7i ramps up.

Overall, we continue to expect most OEMs to be aggressive as market share is the #1 priority. Although there were no big price cuts announced at the Shanghai Auto Show, our view is that there is likely another wave of price cuts to come as industry demand remains soft.

Moreover, the price of lithium carbonate has dropped dramatically this year which provides more cushion on the gross margin side.

April OEM recap

Li Auto delivered 25,681 vehicles (+23% MoM, +516% YoY), beating our forecast and setting a new monthly record. This includes >10,000 units of the L7 in its first full month of deliveries (vs. 7,702 in March).

Xpeng delivered 7,079 vehicles (+17% MoM; -55% YoY), slightly below our expectations. The P7i mid-cycle face-lift should help volume in May/June as management expressed confidence in the order book.

Xpeng officially revealed the G6 at the Shanghai Auto Show last month and this will be the most important product for the company this year to grow sales (double current monthly sales by end of 3Q), set for late June deliveries.

Nio delivered only 6,658 vehicles (-36% MoM, +31% YoY), below our forecast. Demand for ET5 and ES7 appear to be getting weaker sequentially while the rest of the portfolio is undergoing a platform transition (except for ET7 getting an interior upgrade this month).

Deliveries of the new EC7 began on 4/28, a few weeks earlier than anticipated, suggesting operational execution is on track. The new ES6 is expected to begin deliveries toward end of May (Nio's best selling SUV model).

Zeekr delivered sales of 8,101 vehicles (+22% MoM; +279% YoY). The average order value for 001 shooting break sedan is 336k RMB and 009 luxury MPV is 527k. Zeekr's upcoming X model is expected to garner higher relative volumes with starting price of just 190k (deliver in June, targeting 40,000 units for 2023).