Xpeng delivered weak 4Q results, accompanied by a muted 1Q outlook that shows March demand still under pressure, Deutsche Bank said.

Xpeng (NYSE: XPEV) reported weaker-than-expected fourth-quarter earnings today, and as usual, Deutsche Bank analyst Edison Yu's team provided their first impressions.

Here's the full text of the note the team sent to investors today.

Xpeng delivered weak 4Q results (even softer than our preview), accompanied by a muted 1Q outlook that shows March demand still under pressure.

Deliveries for 4Q were already reported at 22,204 units, leading to revenue of 5.1bn RMB, below our 5.4bn and consensus 5.7bn on lower vehicle pricing and "other sales."

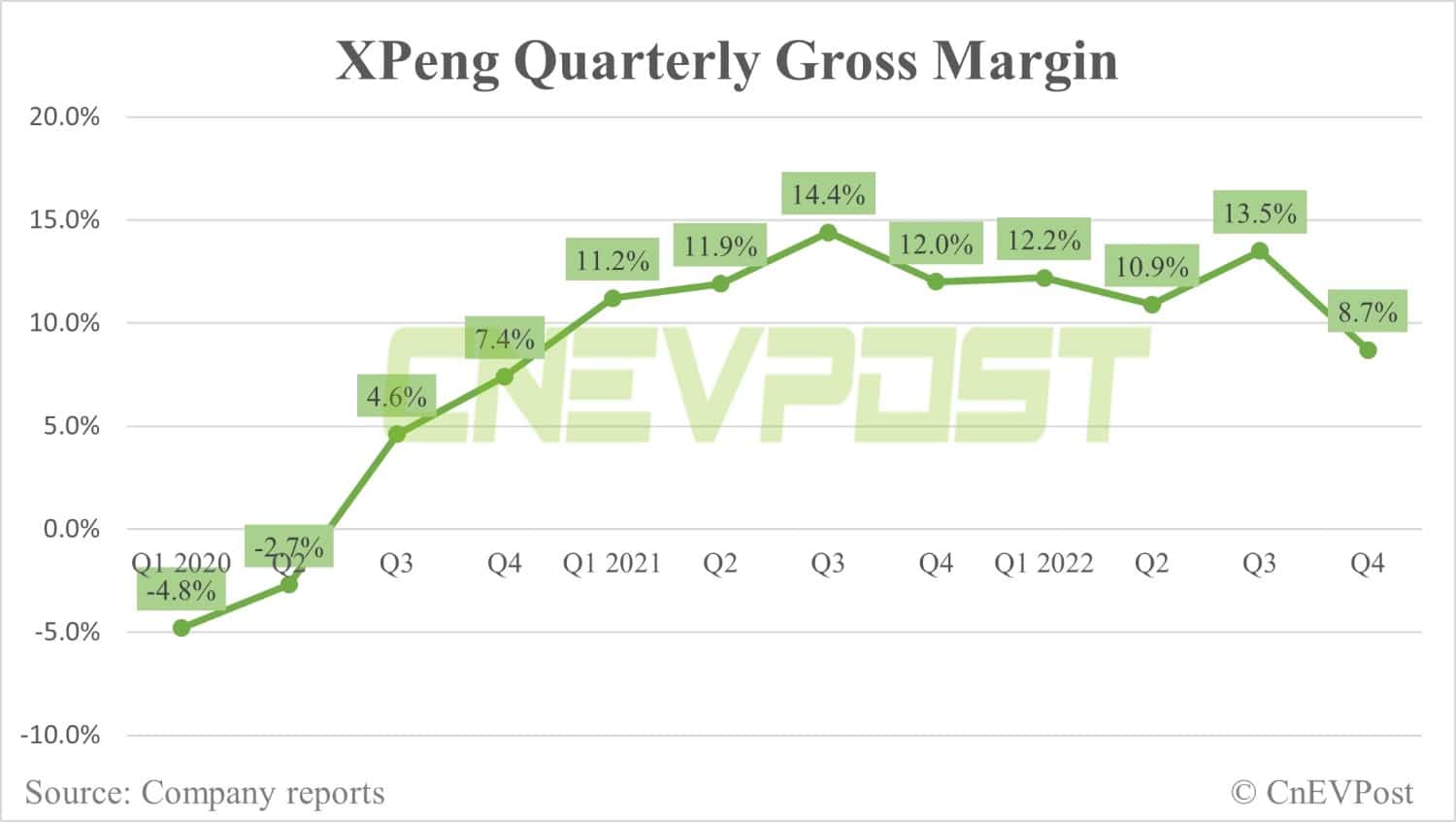

Total gross margin declined 480bps QoQ to 8.7%, missing our 11.5% estimate (consensus 12.1%), driven by much lower vehicle margin (5.7% vs. our 8.5% due to increased promotional activity; lowest since 2H20).

Opex of 2,986m RMB essentially matched our model as lower R&D offset higher SG&A.

All together, EPS of (2.57) came in worse than our (2.33) forecast. Management provided a slightly worse 1Q23 volume guidance than expected, calling for 18,000-19,000 deliveries, vs. our 19,500 forecast (translating into 4.0-4.2bn RMB in revenue).

This would imply March improving MoM to low 7,000 units at the mid-point.

ASP will continue to worsen following price cuts and unfavorable mix (G9 volume struggling).