"Even if we exclude these one-time headwinds, vehicle of margin of 13.5% would have been a miss and lowest since 2Q20," Deutsche Bank said.

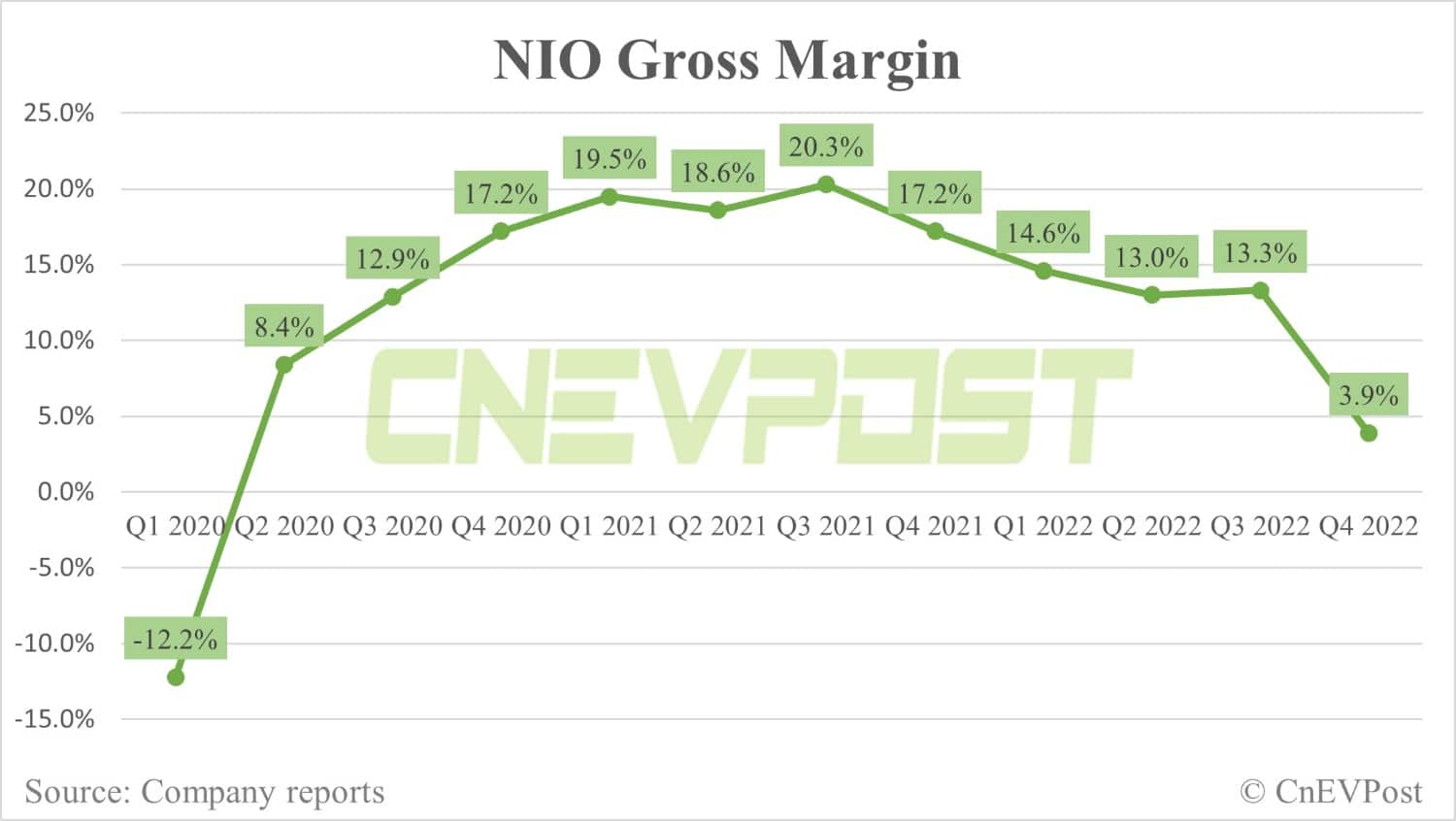

Nio (NYSE: NIO) reported disappointing fourth-quarter results yesterday, in which gross margin fell to low single digits because of model transitions.

In a research note sent to investors yesterday, Deutsche Bank analyst Edison Yu's team noted that Nio's gross margin was just 3.9 percent in the fourth quarter, well below their 13.5 percent forecast and below the consensus estimate of 13.9 percent.

"Even if we exclude these one-time headwinds, the vehicle of margin of 13.5% would have been a miss and lowest since 2Q20," the team wrote.

R&D and SG&A expenses were RMB 7.5 billion, significantly higher than expected due to increased spending on developing new models, technology, and various other factors, Yu's team noted.

Nio guided for first-quarter deliveries of between 31,000 and 33,000 units, implying that March deliveries are expected to be between 10,337 and 12,337 units, flat or down from February.

Nio management believes that doubling sales to over 240,000 units this year is realistic and sees a path to 30,000 deliveries per month once all five new models are launched by the end of the third quarter or early in the fourth quarter.

Yu's team believes this will be difficult to achieve and that investors will not give them any credit now given the recent string of misfires.

Here is the team's first look at Nio's fourth-quarter earnings.

4Q22 Earnings First Look

Nio reported disappointing 4Q results, even worse than we previewed.

Deliveries for the fourth quarter were already reported at 40,052 units, leading to revenue of 16.1bn RMB, vs. our/consensus 16.2bn/17.1bn forecasts.

Gross margin of only 3.9% was significantly below our 13.5% forecast (consensus 13.9%), driven by downside in vehicle margin (6.8% vs. our 16.7%) which was negatively impacted by 6.7% points from inventory provisions, accelerated depreciation, and losses on purchase commitments related to first-gen 866 models.

Even if we exclude these one-time headwinds, vehicle of margin of 13.5% would have been a miss and lowest since 2Q20.

Opex of 7.5bn was materially above our expectations, both on R&D and SG&A, due to greater spending on development of new models/tech and various other factors.

All together, adjusted EPS of (3.07) came in worse than our/ consensus (1.83)/(1.85) estimates.

Management provided a soft outlook for 1Q23, calling for 31,000-33,000 deliveries. This compares to our 34,000 unit forecast and suggests March will be flat/down sequentially as the company sells down old inventory and prepares to launch 4 new models in the second quarter.

This translates into 10.9-11.5bn RMB in revenue, below our 12.3bn forecast on lower volume and pricing.

Looking beyond, management still believes doubling volume this year is realistic (>240k) and sees a path to 30k deliveries per month once all the 5 new models are out by late 3Q or early 4Q.

We think this will be difficult to achieve and don't think investors will give them any credit for this right now given recent string of misfires.

While previously it expected to launch all these models in 2Q, the ET5 shooting brake (touring) version will now be slightly delayed into July.

On gross margin, 1Q will remain challenging with vehicle margin in the single digits most likely but then 2Q should recover back to mid teens and then 18-20% in 4Q assuming benefit from lower battery input costs, pricing/mix, and higher capacity utilization.

R&D is expected to trend around 3-3.5bn (non-GAAP basis) per quarter and SG&A will decline as % of sales for the full-year.

This all translates into "core" Nio breaking even in 4Q23 or about a 1bn Ebit loss on reported basis due to incremental investments related to battery in-sourcing, new mass market brands, smartphone, and chip development.

The company maintains that 2024 will see overall company break-even.

As we previewed last week, we believe Nio is currently facing its greatest challenges since nearly going bankrupt in 2020.

While cash is plentiful, poor execution ramping up ET5 and ET7 production led to material demand destruction as customers grew tired of waiting and simply moved on.

Furthermore, the broader premium segment is not shifting to pure electric as quickly as anticipated, enabling ICE and EREV models to outperform.

As a result, Nio's sales will be quite choppy for most of 1H23 as it attempts to launch multiple new models and rekindle demand for existing NT2.0 cars (ET7, ES7).