The earnings report represents the final reset of numbers before the long-awaited product supercycle takes off and Nio can finally demonstrate the power of its brand and ecosystem.

Nio reported second-quarter revenue that beat expectations on Wednesday, though the loss widened.

As usual, Deutsche Bank analyst Edison Yu's team provided their first impressions of Nio's performance in a research note sent to investors on Wednesday.

The team sees Nio's second-quarter results as mostly solid, especially in terms of gross margin, and offers a better-than-feared outlook for third-quarter sales.

Nio's delivery guidance for the third quarter suggests better-than-feared demand for models based on the first-generation NT 1.0 platform -- the ES8, ES6 and EC6, according to the team.

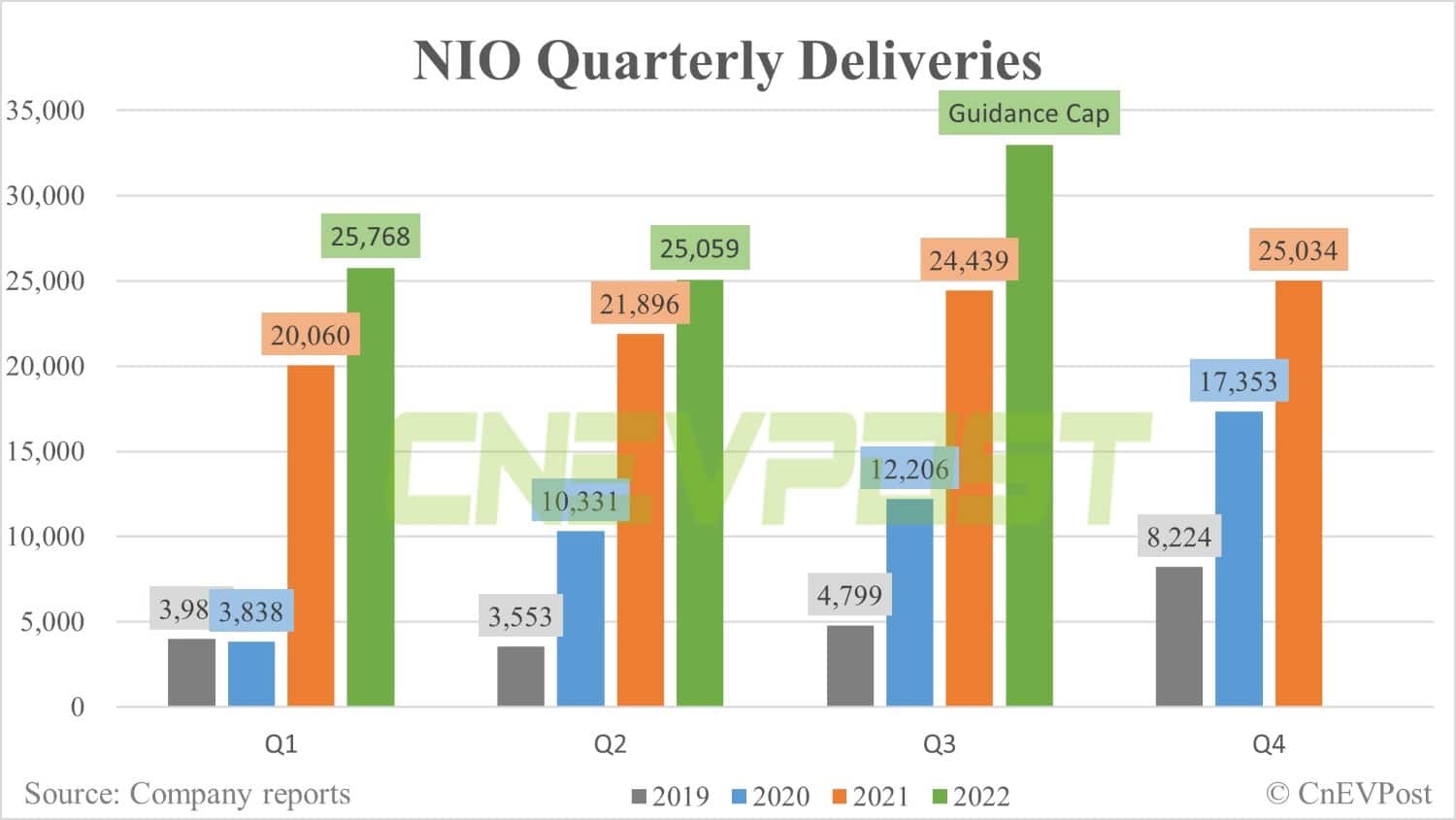

NIO expects Q3 deliveries of vehicles to be between 31,000 and 33,000, representing an increase of about 26.8 percent to 35.0 percent from the same quarter of 2021. https://t.co/i4DAEomTLo

— CnEVPost (@CnEVPost) September 7, 2022

The company's management said during the conference call that deliveries in each month of the fourth quarter would be at record levels, which the team believes paves the way for achieving 55,000-60,000 deliveries for the quarter.

The following is the team's full report.

2Q22 Earnings First Look

Nio reported mostly solid 2Q results, especially on gross margin, while providing a better than feared 3Q volume outlook.

Deliveries for the second quarter were already reported at 25,059 units, leading to revenue of 10.3bn RMB, better than our/consensus 10.1bn/9.8bn forecasts due to stronger ASP/mix.

Moreover, gross margin of 13.0% was above our 12.2% forecast (consensus 12.4%), driven by upside in vehicle margin (16.7% vs. our 15.4%). This appears to reflect some slight benefit from price hikes and favorable ET7 contribution.

However, opex of 4,432m was noticeably above our expectations, both on R&D (new product/tech) and SG&A (marketing and promotion of ES7).

All together, adjusted EPS of (1.34) came in worse than our (1.17) estimate.

Management provided a better than feared outlook for 3Q22, calling for 31,000- 33,000 deliveries, implying 10,300-12,300 for September (translating to 12.8- 13.6bn RMB in sales).

This is above our 30,500 forecast and suggests to us demand for the existing 866 models is holding up relatively better than feared but also the casting supplier issue is still a headwind, albeit improving sequentially.

Nio is working to qualify more suppliers by the end of October, which should enable ET7 sales to hit full 5,000/month capacity.

For 4Q, management indicated it expects to deliver record monthly volume every month with a peak in December that includes 10,000 ET5 units (internal target even higher). This paves a path to 55,000-60,000 deliveries, in our view.

In respect to gross margin, 3Q should see improvement QoQ as Nio benefits from new models and price hikes, suggesting upside to our/ consensus forecasts.

Overall, we continue to believe this earnings represents the final reset of numbers as previewed before the long awaited product supercycle takes off and the company can finally demonstrate the strength of its brand and ecosystem.