- There have been frequent cases of LFP producers receiving large orders, and some of the big players are raising prices.

- Rising demand and product technology iterations are the two main reasons for the recent price hikes, analysts said.

China's lithium industry is seeing a long-awaited respite after major players faced losses due to price slumps over the past few years.

There have been frequent cases of lithium iron phosphate (LFP) producers receiving large orders recently, while at the same time, some big players are raising prices, the Securities Times said in a report today.

"Mainstream LFP makers are now generally seeing an increase in capacity utilization, especially with strong demand for high-end products," the report quoted a lithium battery materials insider as saying.

The fourth-generation LFP production lines of a leading lithium producer in central China is operating at full capacity, the source said.

In the last two months or so, Jiangsu Lopal Tech has received long-term orders from Blue Oval and CATL (SHE: 300750), as well as additional orders from LG Energy Solution, the report noted.

Fulin Precision received long-term orders from CATL in August 2024 to supply at least 140,000 tons per year from 2025 to 2027 to the battery maker.

Additionally, LFP makers including Hunan Yuneng New Energy and Hubei Wanrun New Energy have also said they have been busy with production and sales since the fourth quarter.

Shenzhen Dynanonic said several of its production sites did not halt production during the Chinese New Year holiday to deliver products to customers, the report noted.

Some lithium producers are looking to increase prices. Hunan Yuneng said in mid-January that the company had been actively negotiating with customers and that some have already accepted price increases, according to the report.

Significantly rising market demand and product technology iterations are the two main reasons for the recent price hike of LFP, said Zhai Linlin, a LFP analyst at market researcher OilChem, as cited by Securities Times.

LFP batteries with its cost-effective advantage has become the absolute mainstream of the domestic power battery installed capacity, and the expansion of the market scale will further promote manufacturers to increase R&D, Zhai said.

As market demand turns better, LFP manufacturers' mentality is also changing.

In the past two years, most LFP manufacturers were in the loss-making state, and they are now eager to turn around the loss, the Securities Times quoted Shanghai Iccsino Data senior researcher Zhang Jinhui as saying.

Cases of selling at a loss are now significantly reduced, and manufacturers have greater sentiment to support prices, Zhang said.

Lithium is one of the key raw materials for batteries, which typically account for a large portion of the cost of an electric vehicle (EV) model.

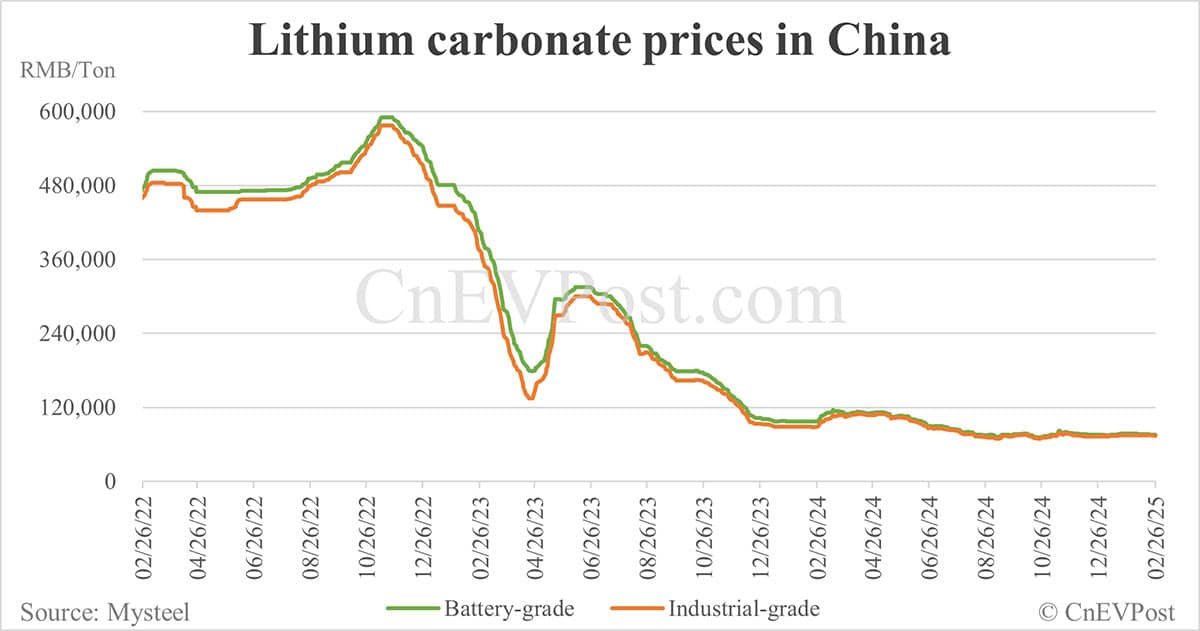

Lithium prices saw a wild ride in China in 2022, with the price of battery-grade lithium carbonate rising to RMB 590,000 ($81,170) per ton in November of that year, up about 14 times from RMB 41,000 per ton in June 2020.

After that, however, the price of lithium carbonate saw a prolonged decline, and battery-grade lithium carbonate is now priced below RMB 80,000 per ton in China.

Lithium carbonate and iron phosphate are the main raw materials for LFP.

($1 = RMB 7.2685)