Deutsche Bank said Nio's third-quarter delivery guidance is below their expectations, which could mean that new order flow will be hard to sustain after the initial surge.

Nio (NYSE: NIO) reported its second-quarter earnings today, and as usual, Deutsche Bank analyst Edison Yu's team shared their first look.

Here's what the team said in a research note sent to investors today.

2Q23 Earnings First Look

Nio reported soft 2Q results as previewed with a weaker-than-expected 3Q outlook.

Deliveries for the second quarter were already reported at 23,520 units, leading to revenue of 8.8bn RMB, below our/consensus 9.1-9.2bn forecasts, hurt by lower ASP.

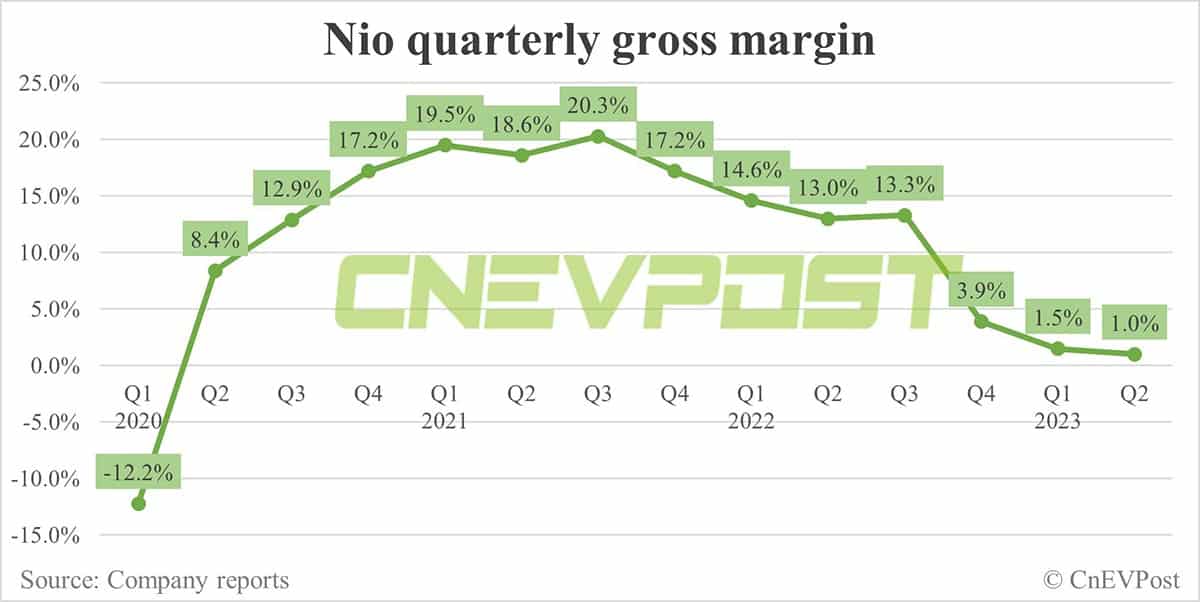

Gross margin of 1.0% was below our 2.2% forecast (consensus 3.3%), driven by both vehicle margin (6.2% vs. our 6.5%) and "other sales" (-22.7% vs. our -20.0%).

Opex of 6.2bn was a bit above our expectations, mainly on R&D.

All together, adjusted EPS of (3.28) came in worse than DBe/consensus around (2.85).

Management provided a weaker-than-expected outlook for 3Q23, calling for 55,000-57,000 deliveries (18.9-19.5bn RMB in revenue). This compares to our 60,000 unit forecast and suggests Aug/Sep will, on average, be lower relative to July's 20,462.

While some of August's weakness can be attributed downtime for a production line upgrade, we are surprised there isn't a stronger rebound in September.

This likely means new order flow is proving difficult to maintain after the initial surge and the new EC6 probably won't be a meaningful contributor.

On the earnings call, we will look for further insight on the ability to maintain/exceed 20,000 deliveries per month going forward, the trajectory of vehicle margin in 2H, and openness to strategic actions.