Xpeng reported second-quarter earnings today, and Deutsche Bank analyst Edison Yu's team provided their first impressions.

Xpeng reported second-quarter earnings today, and Deutsche Bank analyst Edison Yu's team provided their first impressions.

Here's what they had to say in their research note.

Xpeng delivered soft 2Q results, but provided a solid outlook for 3Q, demonstrating strong G6 contribution.

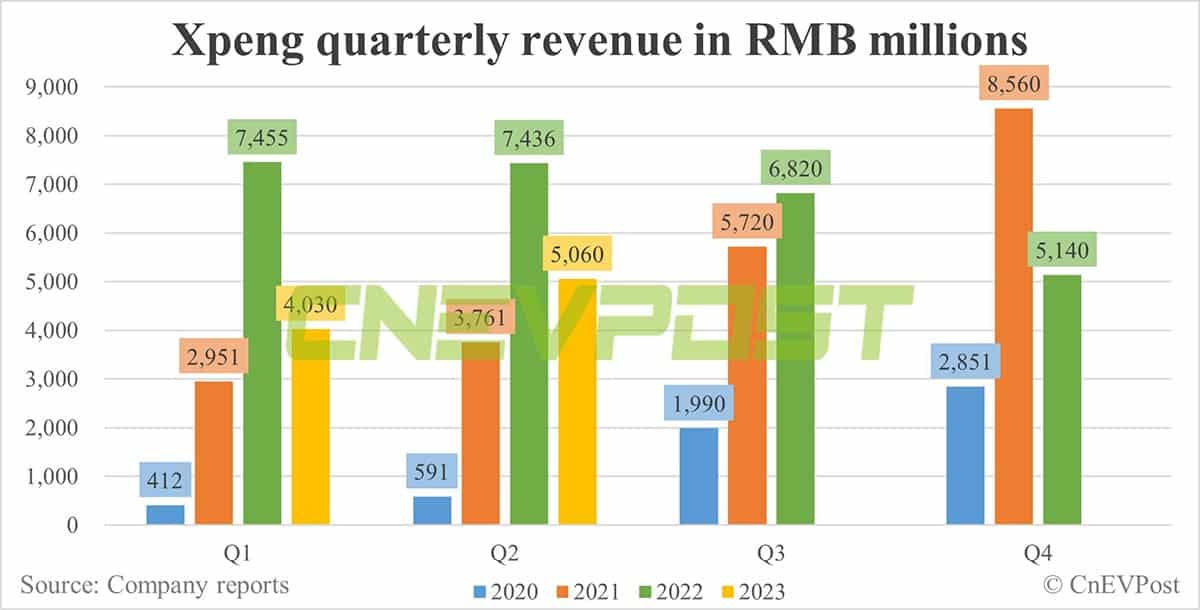

Volume for 2Q23 was already reported at 23,205 units, leading to revenue of 5.06bn RMB vs. consensus/DBe 4.8-4.9bn estimate; ASP was slightly better than anticipated.

Gross margin surprised to the downside, declining 560bps QoQ to -3.9%, missing our 2.5% estimate, driven by lower vehicle margin of -8.6% vs. our -1.1%.

Vehicle margin was negatively impacted by inventory write down on G3i (-450bps) and aggressive promotional activity.

Opex of 2,911m was largely consistent with our estimates.

All together, EPS of (3.10) came in below our (2.64). Cash use in the qtr was <1bn, better than our model.

Management provided a solid 3Q23 outlook, calling for 39,000-41,000 deliveries, in-line with our 40,750 forecast, translating into 8.5-9.0bn RMB in revenue (below our 9.6bn).

This implies Aug/Sep seeing material MoM improvement as July garnered 11,088 units while suggesting weaker ASP/mix than we anticipated.

On the earnings call, we will look for further commentary on the G6 production ramp and vehicle margin dynamics in the 2H.