CATL's battery installed base grew 59.6 percent year-on-year in January-May, while BYD's grew 107.8 percent year-on-year, according to SNE Research.

China's CATL and BYD (OTCMKTS: BYDDY) continued to dominate the global power battery market in the January-May period, the latest figures show.

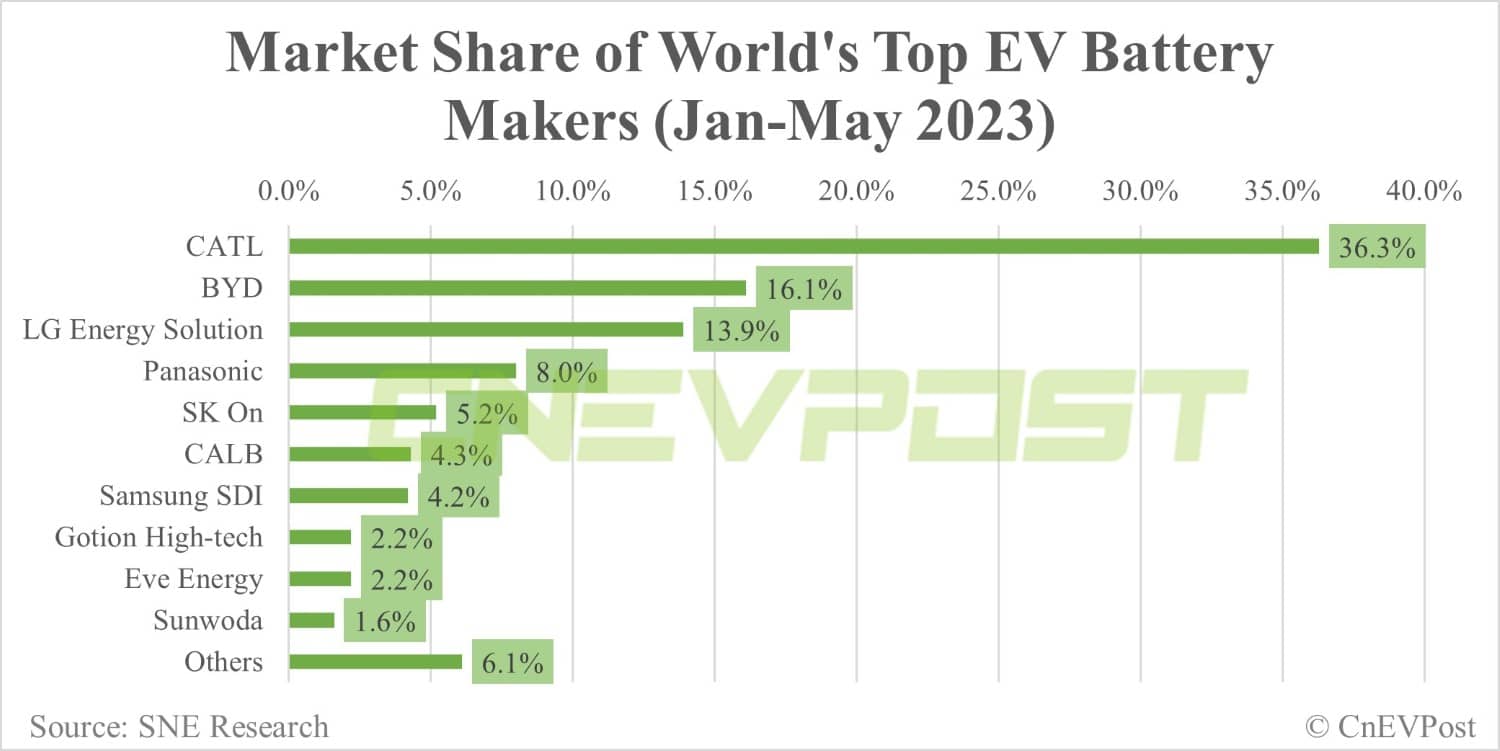

From January to May, total global battery consumption for electric vehicles (EVs) was 237.6 GWh, up 52.3 percent from 156.0 GWh in the same period last year, according to data released today by South Korean market research firm SNE Research.

CATL installed 86.2 GWh of batteries in January-May, up 59.6 percent from 54.0 GWh in the same period last year.

The Chinese power battery giant continues to rank first in the world with a 36.3 percent share and remains the only battery supplier in the world with a market share of more than 30 percent.

This is up from its 34.6 percent share in the same period last year and up from its 35.9 percent share in the January-April period.

CATL's batteries are installed in many major passenger EV models in China's domestic market, such as the Tesla Model 3, Model Y, SAIC Mulan, GAC Aion Y, and Nio ET5, as well as Chinese commercial vehicle models, and continue to grow steadily, SNE Research said.

BYD installed 38.1 GWh of power batteries from January to May, up 107.8 percent from 18.4 GWh in the same period last year.

The company ranked second with a 16.1 percent share from January to May, up from 11.8 percent in the same period last year and unchanged compared to January-April.

BYD has gained popularity in China's domestic market with its competitive pricing by establishing a vertically integrated supply chain management, including battery self-sufficiency and vehicle manufacturing, SNE Research said.

With the launch of the Atto 3 model, BYD showed explosive growth by expanding its market share outside of China in Asia and Europe, SNE Research said.

LG Energy Solution installed 33.0 GWh of power batteries from January to May, up 56.0 percent year-on-year.

The South Korean company ranked third in the world with a 13.9 percent share, slightly up from 13.6 percent a year ago and down from 14.1 percent in the January-April period.

Panasonic of Japan ranked fourth with an 8.0 percent share, SK On of South Korea ranked fifth with 5.2 percent share and CALB of China ranked sixth with a 4.3 percent share.

Samsung SDI of South Korea, China's Gotion High-tech, Eve Energy, and Sunwoda ranked seventh, eighth, ninth, and tenth respectively, with 4.2 percent, 2.2 percent, 2.2 percent, and 1.6 percent shares in January-May.

It is worth noting that CALB's power battery installed base of 10.2 GWh continued to be higher than Samsung SDI's 9.9 GWh in January-May.

From January to March, CALB's 5.7 GWh was lower than Samsung SDI's 6.5 GWh. From January to April, CALB's 8.4 GWh exceeded Samsung SDI's 7.5 GWh.

In 2023, Chinese companies are expected to push into overseas markets such as Europe, preparing for a gradual decline in growth in China's domestic market, SNE Research said.

Europe is the largest EV market after China and is aggressively implementing environmental policies, so it is highly likely to be the biggest battleground in the future, according to SNE Research.

In the future, the proportion of LFP batteries in Europe is expected to increase as Chinese companies enter the European market in earnest, the report said.