"Xpeng delivered even softer 1Q23 results than we previewed, accompanied by a muted 2Q outlook," Edison Yu's team said.

Xpeng (NYSE: XPEV) reported weaker-than-expected first-quarter earnings today, and as usual, Deutsche Bank analyst Edison Yu's team provided their first look.

Here is the research note the team sent to investors today.

1Q23 Earnings First Look

Xpeng delivered even softer 1Q23 results than we previewed, accompanied by a muted 2Q outlook.

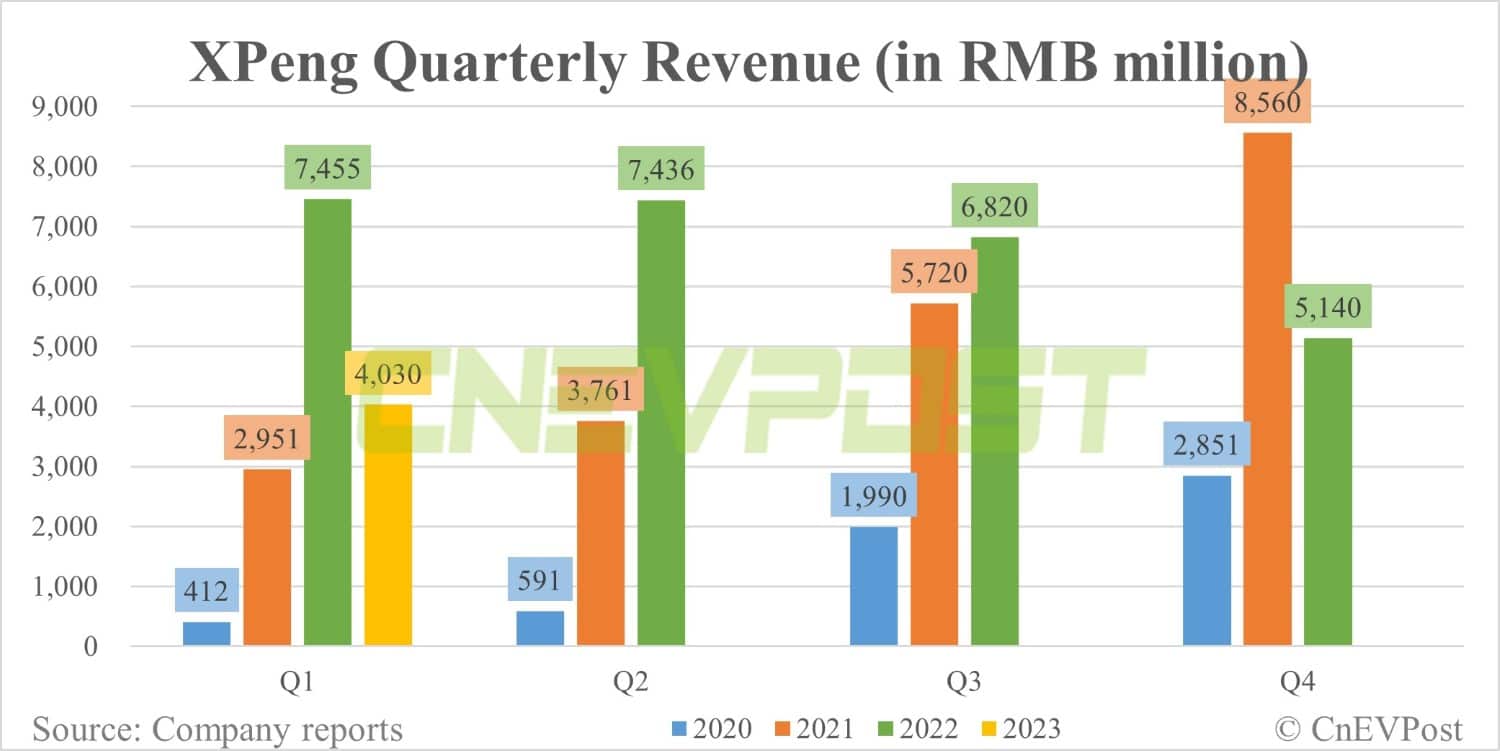

Volume for 1Q was already reported at 18,230 units, leading to revenue of 4.03bn RMB, essentially in line with our 4.04bn estimate; vehicle pricing was slightly lower, offset by "Services and other."

Total gross margin declined 700bps QoQ to just 1.7%, missing our 5.0% estimate (consensus 6.1%), driven by lower vehicle margin (-2.5% vs. our 0.4% due to aggressive price cuts/promotions).

Opex of 2,654m came in below our model as higher R&D was offset by lower SG&A.

All together, EPS of (2.57) came in about in line with our (2.52) forecast.

Management provided a muted 2Q23 outlook, calling for 21,000-22,000 deliveries, vs. our 24,000 forecast, translating into 4.5-4.7bn RMB in revenue (vs. our 5.6bn).

This implies May/June seeing little to no MoM improvement as April garnered 7,079 units and pricing/mix facing further pressure (G9 demand still struggling and P7i constrained by component supply).

On the earnings call, we will look for further commentary on the exact timing of G6 deliveries (SOP seemingly has already begun), pricing, and volume expectations.