Deutsche Bank analyst Edison Yu's team expects sales of EVs to fall across the board in April and may also be affected in May, leading to a broad downward revision of second-quarter volumes.

China's control measures against the latest wave of the Covid pandemic are exposing the new energy vehicle (NEV) chain to supply disruptions. In Deutsche Bank's view, April could be a lost month for electric vehicle (EV) companies in terms of sales.

"Based on our channel checks and conversation with companies, the Covid situation in China is becoming much more disruptive than we anticipated even just a week ago," Deutsche Bank analyst Edison Yu's team said in a research note sent to investors on Monday.

China on Sunday added 1,164 new local confirmed cases of Covid and 26,345 new asymptomatic infections, according to health authorities.

The vast majority of those cases were reported in Shanghai, home to Nio's global headquarters and Tesla's China factory, which added 914 new locally confirmed Covid cases and 25,173 new locally asymptomatic infections on Sunday.

Shanghai has been in a phased lockdown since March 28, and Tesla Giga Shanghai has been shut down since then.

Hefei, where the Nio (NYSE: NIO, HKG: 9866) plant is located, did not go into lockdown, but the EV maker said on Saturday that the company had also suspended production as Covid caused partners in the supply chain to shut down production.

While initially contained mostly in Shanghai, several other major cities could be at least partially locked down in the next few days or weeks, and EV production will be severely limited, if not halted, Yu's team said.

The team now expects sales of EVs to fall across the board in April and may also be affected in May, leading to a broad downward revision of sales in the second quarter.

The situation is fluid and varies by the automaker. The team said they will be watching local developments and this is their latest assessment:

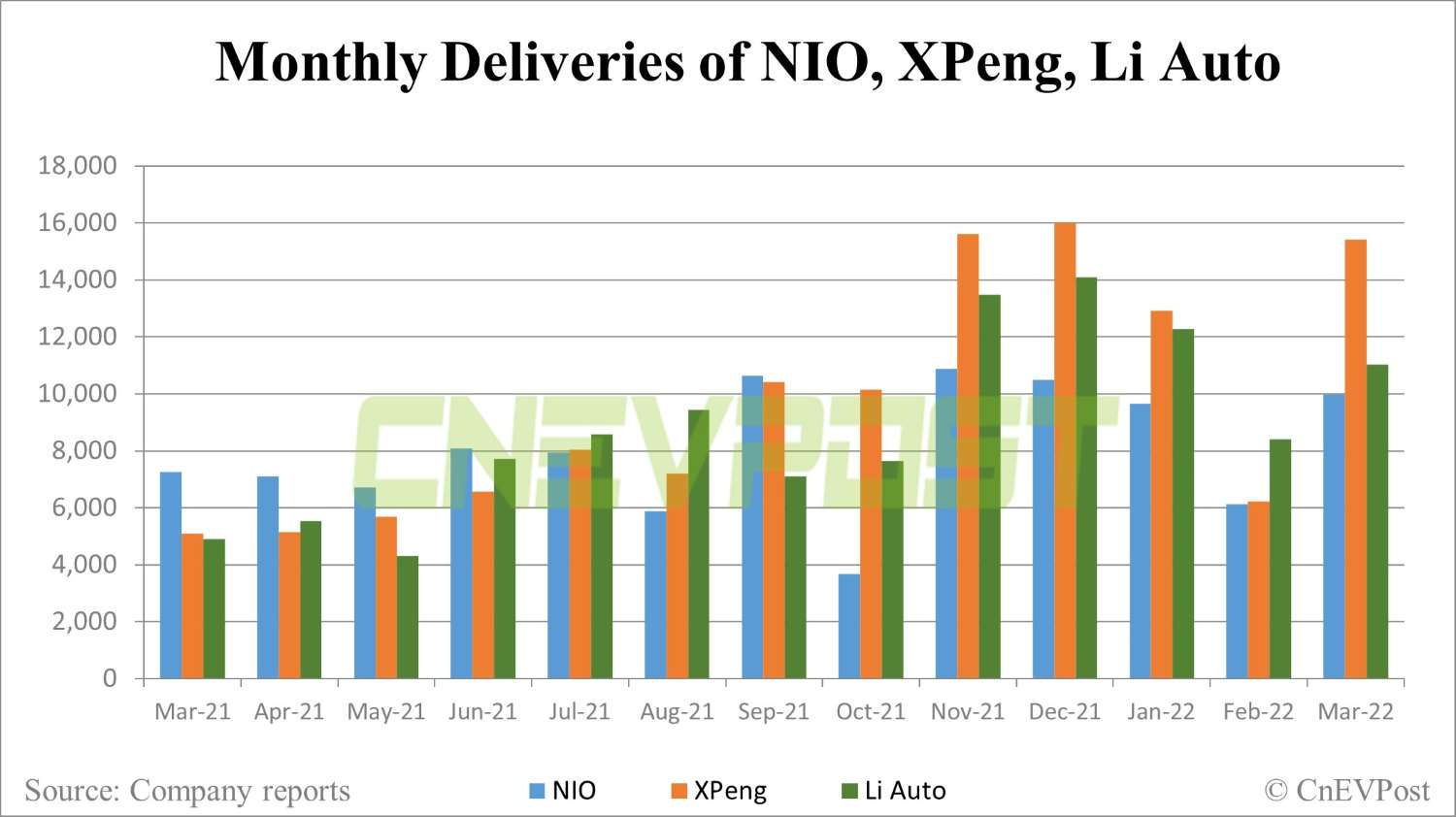

Nio: announced a production stoppage on Saturday (4/9) as it ran out of certain parts (mainly traditional components related to exterior and engineering and we suspect some low end Bosch chips as well) caused by suppliers in Shanghai, Jilin, and Jiangsu.

In addition, Nio announced a 10,000 RMB price hike for its current gen vehicles to combat rising raw material prices (BaaS subscription price also going up) but maintained price on new NT2.0 vehicles (ET7, ET5).

These price hikes will kick in on new orders placed starting 5/10. And we think at this moment, the new ES7 SOP will not be delayed (official unveil likely postponed until mid-late May) but the risk grows the longer the COVID lockdowns drag on. Our April delivery estimates likely need to come down by 60-65%.

Xpeng: we hosted management last Thursday and production had not been adversely impacted up to that point and exposure to Shanghai was low (~1,000 units per month).

The company highlighted it now has 3 battery cell suppliers (CATL, Eve, CALB) and developed several alternative suppliers for lower-end MCU chips. Xpeng already raised price last month by 10,000/20,000.

Going forward, we think southern China may get hit by these COVID lock downs and/or supply chain simply becomes too challenging. Our April delivery estimates may need to come down by 25-35%.

Li Auto: LI already saw some relatively small challenges in March related to supply chain which we think were related to Bosch ESP (and perhaps some traditional auto components).

Going forward, we think Li Auto likely will face similar logistical and supply chain challenges as others but could manage through situation better given strong track record of stable execution.

The stock likely outperforms in these type of uncertain environments considering it has highest margin/cash flow and "cheapest" valuation.

Furthermore, it is not as exposed to rising battery input costs (lithium carbonate) as its EREV model uses a small pack. Our April delivery estimates may need to come down by 25-35%.

Notably, though, Yu's team believes that looking beyond to the recent turmoil, the broader EV momentum is very much intact, even if overall auto demand remains weak due to macro pressures.

In other words, the mix shift away from internal combustion engine vehicles is more than enough to offset broader auto sales weakness, the team said.

"For example, last month according to the CPCA, China saw NEV retail sales increase 146% YoY to 455k units while overall auto sales declined 10%, pushing penetration to all time high of nearly 30%," Yu's team noted.