Soochow Securities believes Li Auto's unique product positioning should allow it to enjoy a higher valuation premium than its peers.

Chinese brokerage Soochow Securities initiated coverage on Li Auto with a Buy rating on Monday without giving a price target.

There is mega market space in the smart electric vehicle (EV) industry, and smart product penetration is expected to continue to exceed expectations, Soochow Securities said, adding that Li Auto's product deliveries are expected to continue to grow and the company should enjoy a higher valuation premium than peers.

Soochow Securities' team researched Li Auto's executive team and concluded that its founder, Li Xiang, has the ability to quickly capitalize on market opportunities as a successful serial entrepreneur.

Li Auto's only model currently on sale, the Li ONE, has managed to become a hit through its unique positioning and selling point of solving mileage anxiety, the team noted.

"Over the next 5-10 years, Li Auto's focus on family car needs is in line with future economic operating trends and is expected to achieve a sustained increase in sales scale," the team wrote.

Because vehicles with extended-range technology do not have mileage anxiety issues, Li ONE has greater acceptance in Chinese cities that do not restrict car purchases, and therefore has more room for future sales ramp-up, the team said.

Li Auto is building on its original platform using extended-range technology with the high-voltage all-electric platform Whale as well as Shark, both of which support 800V, with the former focusing on space and the latter on performance.

The company's goal is to build EVs that can get 400km range in 10-15 minutes of charging, the team noted.

Soochow Securities believes that in the short term, China's charging infrastructure is not being built at the same rate as the growth in sales of pure electric models, so there could be a shortage of supply of charging facilities.

Li Auto's vehicles with extended-range technology, on the other hand, are expected to see continued sales growth as they meet China's national new energy vehicle development plan while providing consumers with a great travel experience, the team said.

In the long term, pure EVs are expected to become mainstream products from 2025-2035, when vehicle intelligence will increase significantly and L3 and L4 assisted driving will become popular.

By then, Li Auto's pure electric models based on the Whale and Shark platforms are expected to continue to meet consumer demand and drive sales up steadily, according to Soochow Securities.

The team expects Li Auto to sell 82,000, 170,000 and 420,000 units from 2021-2023, with Li ONE sales of 82,000, 130,000 and 160,000 units, respectively.

They expect Li Auto's gross margins to be 19.28 percent, 21.81 percent, and 23.27 percent from 2021-2023, respectively, and to increase further as its sales volume increases.

The team expects Li Auto's revenue to be RMB 23.6 billion, RMB 51 billion and RMB 116.1 billion, respectively, and net profit attributable to the parent company to be -RMB 1.175 billion, -RMB 690 million and RMB 2.031 billion, respectively, for 2021-2023, corresponding to a PS valuation of 9x, 4x and 2x, respectively.

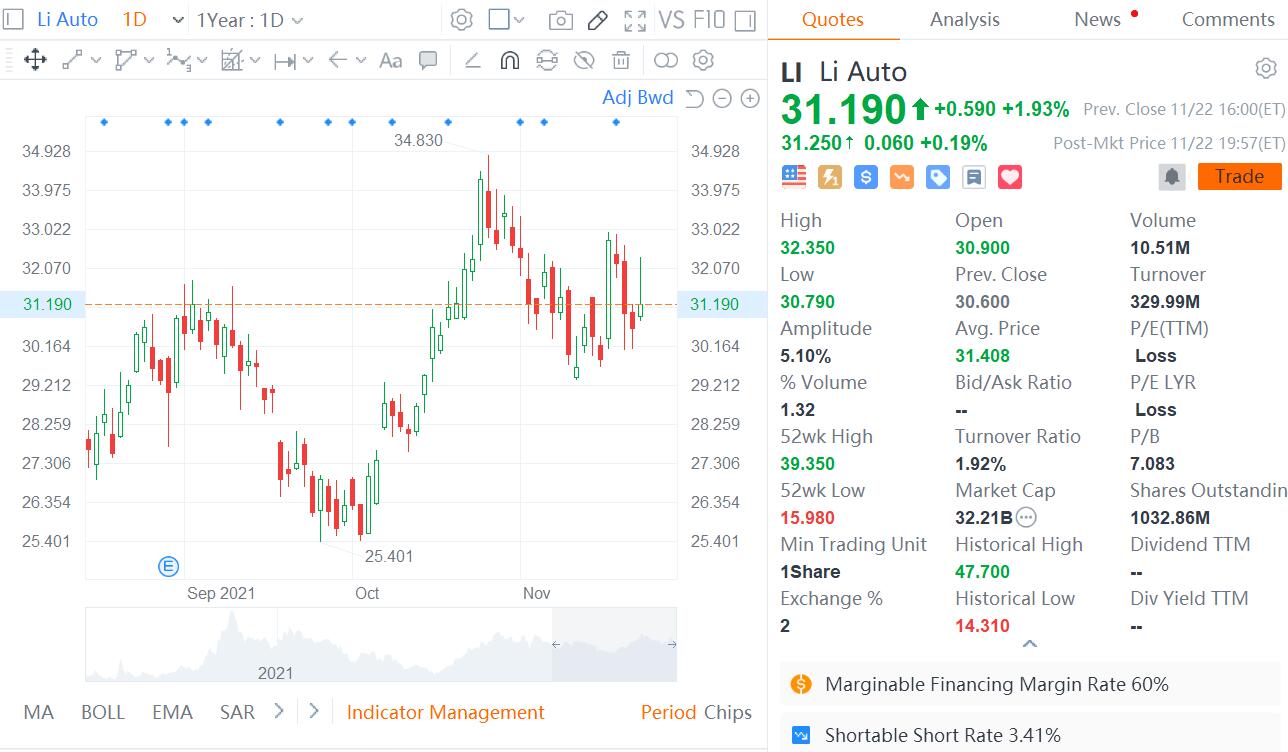

Li Auto rose 1.93 percent to $31.19 at the US close Monday, and it's up about 19 percent since October.

Become A CnEVPost Member

Become a member of CnEVPost for an ad-free reading experience and support us in producing more quality content.

Already a member? Sign in here.