On July 7, 2021, Xpeng was listed on the main board of the Hong Kong Stock Exchange under the code '9868.'

- We estimate Xpeng's 2022 revenue to show the value of the stock.

- The methodology includes the forecast of sales of P7, G3&G3i and the upcoming P5 and SUV models.

- The results indicate that the stock is currently fairly priced.

- Risks primarily come from supply chain and market regulation, but remain controllable.

With the current global chip shortage, most major auto OEMs have suffered from a lack of electronic supplies. Amid these concerns, China's EV sales are burgeoning, with light EV sales hitting 241,000, or 15% of total light vehicles sales in June, 2021.

Among the country's EV pioneers, Xpeng (XPEV:NYSE) has recently presented some positive results: its half-year delivery number has surpassed last year's figure.

This article presents a forecast of the company's EV sales in 2022 and evaluates its stock by analyzing each model of Xpeng and using the valuation multiples.

Model-level breakdown

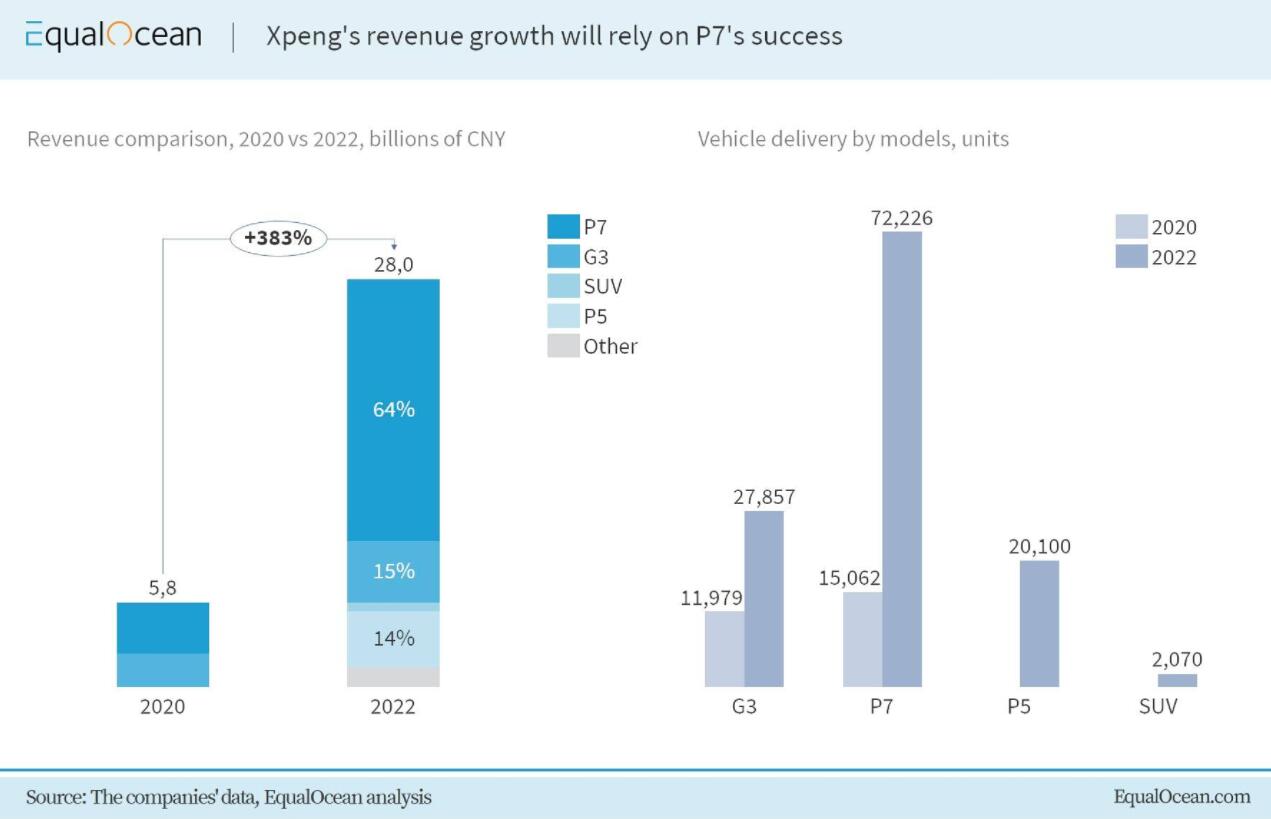

P7 is Xpeng's hit product. Simplifying the modelling, we project the sales of P7 to increase by 184, 100 and 50 units month-on-month until 2023; 184 is the average monthly increase since the model's launch, while the incremental decrease is due to the upcoming P5 and 2022 SUV models. The average selling price will be around CNY 250,000, the same as in 2020.

G3&G3i are the oldest models of Xpeng. The updated version G3i transformed into a more unified family design and attracted more sales. We estimate G3 and G3i will keep lifting sales volume by 46 per month during the same period. The average selling price will be around CNY 150,000 per unit.

P5 will shoulder the company's expectations to become a family sedan. We estimate P5's first-month delivery number in October will be at around 1,000, referring to P7's data. Then the delivery figure will increase by 143 units per month, of which 100 will be at the cost of P7 sales declining, as the two models compete with each other, and 43 is organic growth. Based on the official price starting from CNY 160,00 to 230,000, we predict the ASP will be at CNY 190,000.

Xpeng is planning to launch a new SUV model. The SUV has a family design 'X' logo that brings its length to 4,800 mm. The car design shares the same platform as the P7, the Edward platform. In addition, it will be equipped with premium specifications like XPilot 4.0 and air suspension.

Some industry experts predict the price will be around CNY 300,000. We assume Xpeng will finish its launch day by September 2022. The first-month sale will be 300 units, which will increase by 145 units per month similar to the sales trajectory of Nio's ES6.

Apart from EV sales, other services will account for 5% of total revenue. The 2022 EV sales won't be significantly impacted by the chip shortage.

To sum up, Xpeng's 2022 revenue is projected to reach USD 4.3 billion (CNY 28 billion). Specifically, the company will sell 122,253 vehicles to make USD 4.1 billion topline, and USD 0.25 billion will be from other services.

According to the Street's expectations, the stock is priced at 16, 8.8, 5.6, 4, 2.9 forward PS ratios by 2025. We select 9x as the 2022 multiples. Thus, the market cap will be USD 38.7 billion, around 10% up from the market cap on July 27, 2021.

Risks

Although the expectations for Xpeng are rather bright, the whole industry is facing the chip shortage problem – that is also the biggest threat to Xpeng. For NEV companies, production is challenging while orders are packed.

Through our research, we found that most auto stakeholders in China expect the imbalance to last through 2021, affecting the global light-vehicle sales by 2.5-5.0%, but recover slightly in 2022.

The edtech sector's regulatory update drove the recent sell-off in Chinese concept stocks. However, this crackdown won't be a long-term issue for EV innovators like Xpeng. According to Bloomberg, the government's motivation is to cut family workloads to turn the declining birth rates up.

On the other hand, the 'Made in China 2025' scheme supports EV development radically. So the policy will rather play a positive role in the new energy vehicle market in the long term.

Conclusion

Up to the present, Xpeng has been on the right track, leveraging business through unified family designs, new stores opening, capacity boost and charging facilities build-up. The company's 2022 revenue would be a realistic basis for stocks to start.

The most significant potential risk at present is the capacity problem caused by supply chain shortages. Investors should keep an eye on this topic in the company's upcoming Q2 earnings conference.

This article was first published by Niko Yang and Ivan Platonov on EqualOcean, an investment research firm focusing on China.