With sales near the low end of guidance, Li Auto's performance in the first quarter is expected to be somewhat mixed, but the outlook for delivery in the second quarter will be robust, according to Edison Yu's team.

(Image credit: CnEVPost)

Li Auto (NASDAQ: LI) will report its unaudited financial results for the first quarter on Wednesday, May 10, before the US markets open. As usual, Deutsche Bank analyst Edison Yu's team provided their preview.

Li Auto continues to be the best-performing Chinese electric vehicle stock this year, which is well deserved, though it is expected to have a somewhat mixed quarter as sales approached the lower end of the original outlook, Yu's team said in a research note sent to investors today.

The automaker's management team took advantage of strong initial orders from customers in the premium SUV segment to quickly increase deliveries of new models, the team noted.

Yu's team expects a robust delivery outlook for Li Auto in the second quarter, supported by wide availability of the Li L7 and lower-priced versions of the Li L7 and Li L8.

"Positioning-wise, Li Auto remains the clear favorite in the group and likely stays there unless evidence of softening demand emerges later in the year," the team wrote.

First-quarter earnings preview

Yu's team expects Li Auto to report revenue of RMB 17.7 billion yuan in the first quarter, with a gross margin of 20.7 percent and adjusted earnings per share of 0.40.

The team's model assumes an increase in operating expenses relative to the fourth quarter.

This compares to the current analyst consensus estimates of RMB 18.9 billion, 20.5 percent and 0.49, respectively, in a Bloomberg survey.

Yu's team expects Li Auto's vehicle margin to increase by just 50 basis points sequentially, as average selling prices come under some pressure.

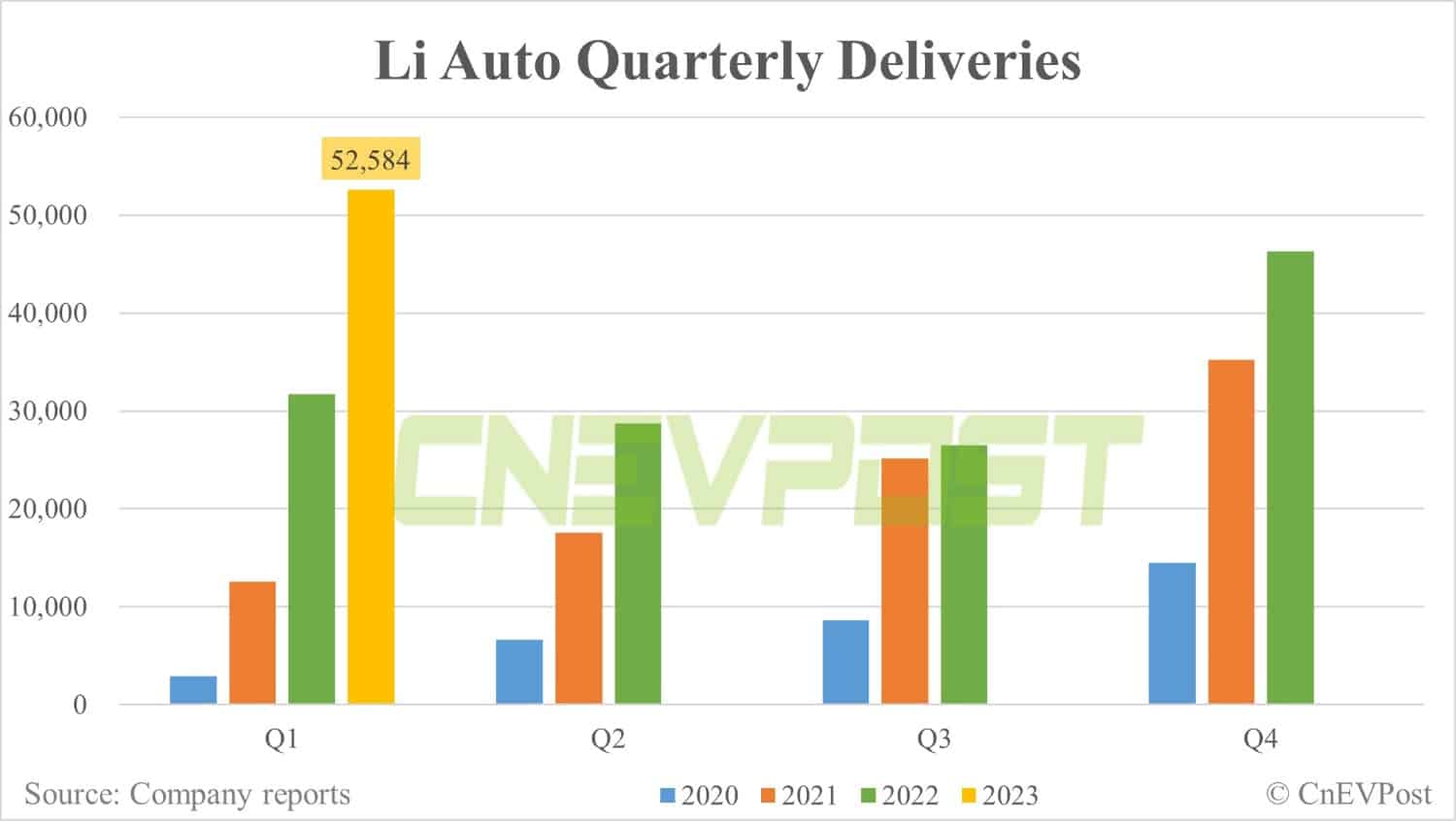

Li Auto delivered a record 52,584 vehicles in the first quarter, near the lower end of its previously provided guidance range of 52,000 to 55,000 vehicles.

Its revenue guidance for the first quarter was RMB 17.45 billion to RMB 18.45 billion, implying year-on-year growth of 82.5 percent to 93 percent.

Gearing up for big second quarter

For second-quarter delivery guidance, Yu's team expects Li Auto's management to target around 75,000 units, supported by deliveries of the Li L7 throughout the quarter and wide availability of the cheaper Air versions of the Li L7 and Li L8.

Li Auto launched the Li L7, its first five-seat SUV, on February 8.

The Li L7 is the least expensive in its product array, with Pro as well as Max versions starting at RMB 339,800 and 379,800 respectively. The Li L7 is available in a lower-priced Air version, starting at RMB 319,800.

Deliveries of the Li L7 Pro and the Li L7 Max began on March 11, and deliveries of the Li L7Air began in late April.

Li Auto is also offering an Air version of the Li L8, with a starting price of RMB 339,800. The Li L8 was previously available in Pro and Max versions with starting prices of RMB 359,800 and RMB 399,800, respectively.

Li Auto's other model, the flagship Li L9, is currently available only in the Max version, with a starting price of RMB 459,800.

Compared to Nio (NYSE: NIO), Li Auto has launched its latest model very efficiently, capturing the initial wave of demand, which is very important in a highly competitive market driven increasingly by product cycles, Yu's team said.

In terms of gross margin, the team expects improvement on a sequential basis as production scales up and battery input costs fall.

Li Auto CFO is conservatively aiming for a gross margin of above 20 percent, given battery costs and a volatile macro backdrop, Yu's team noted, adding that they see 22 percent-23 percent as more realistic, with further upside dependent on battery input costs and average selling prices.

The real test for the company will come later this year, when it will struggle to maintain demand momentum with its three relatively large EREV SUVs in the face of increased competition, the team said.

Some cannibalization will naturally occur among Li Auto's models, but that will likely be offset by share gains from legacy foreign brands, Yu's team said.

The Li L9 sales have already dropped from 10,582 units in December to 5,831 units in March. Since September, foreign brands have lost about 7 percentage points of market share in the premium SUV segment, the team said.

The slow recovery in Chinese auto sales in recent months is something Yu's team attributes to customers prioritizing spending elsewhere after the Covid reopening and recognizing that car prices could fall further, and therefore not rushing to buy.

China's car sales have been slow to recover in recent months, and Yu's team attributes that to customers prioritizing spending elsewhere after the Covid reopening and recognizing that car prices could fall further and therefore not rushing to buy.

In terms of positioning, Li Auto remains the most popular of the Chinese EV startups and is likely to stay there unless there are signs of softening demand or a decline in execution, the team said.